Global financial markets are reacting sharply to ongoing geopolitical tensions in the Middle East. Recent escalations have disrupted energy supply routes, creating unwanted uncertainty in the EU.

The Netherlands sits at the center of the economic shift and can be heavily impacted by global energy prices. The tech-heavy AEX has reacted to the global uncertainty, and with energy costs climbing, inflation expectations and growth are shifting towards a revised downward trend.

In this post, we break down the impacts of geopolitical uncertainty on the Dutch economy, how revised forecasts account for a limited conflict, and whether economic growth and the AEX performance can adjust to the global situation.

The oil shock

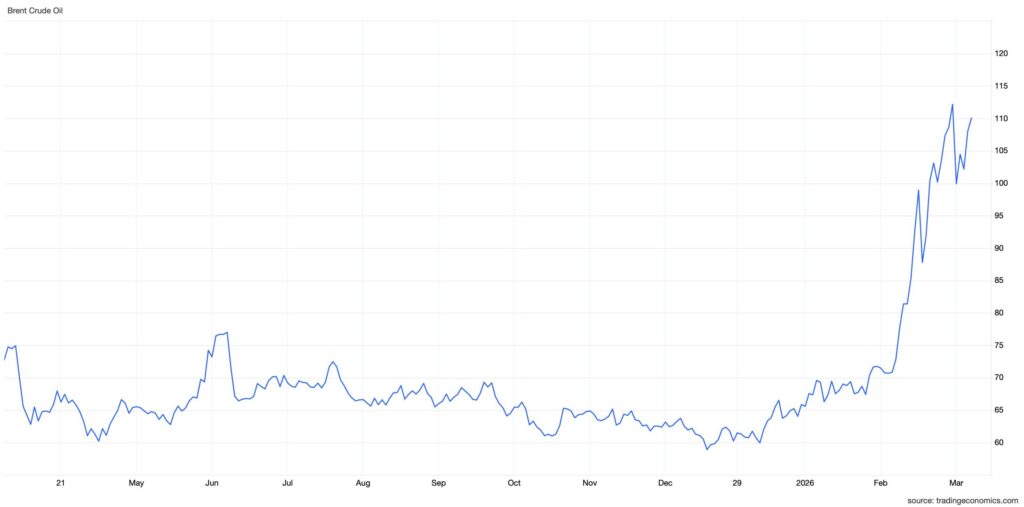

The immediate financial consequence of the Middle East conflict is a severe shock to energy markets. As we reported in a previous article, Brent crude oil has experienced significant volatility, spiking above $100 per barrel.

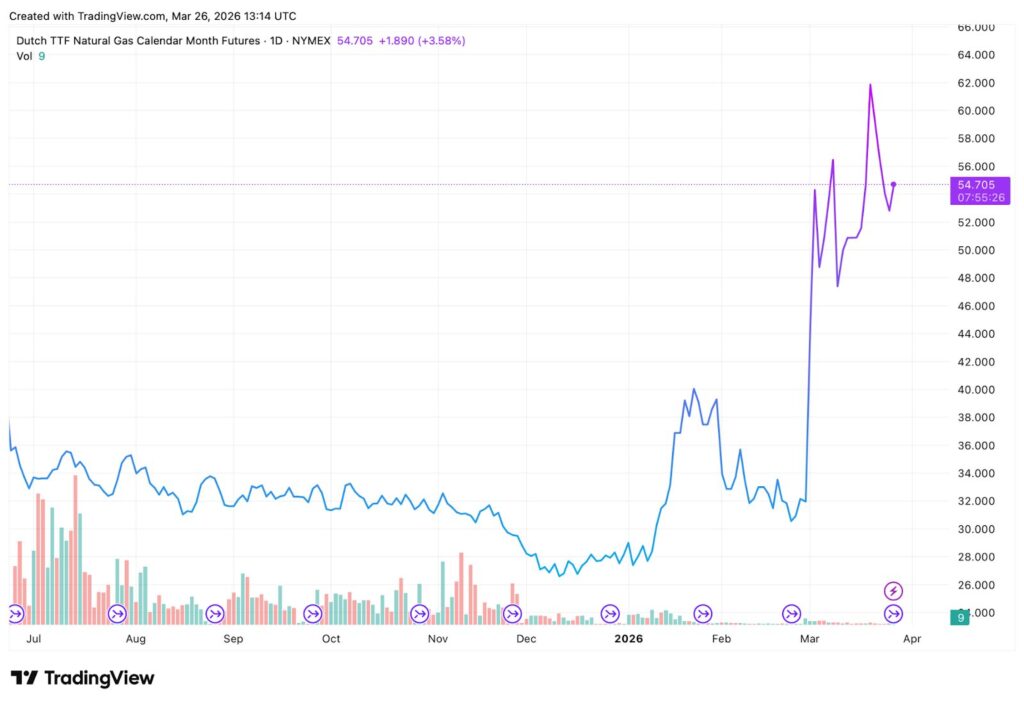

At the same time, gas prices across Europe have also spiked. Reports highlight that the Dutch TTF benchmark soared by 60% due to supply chain shortages of LNG. The TTF benchmark, which tracks gas reselling, spiked over €60 on Tuesday. On a European level, gas price futures spiked by 25% this week to over €68, signaling panic among investors.

As a result, European leaders are considering releasing strategic oil reserves to contain prices and stabilize the market. While it can have short-term positive effects, the IEA, which holds over 1.2 billion barrels, can provide a buffer.

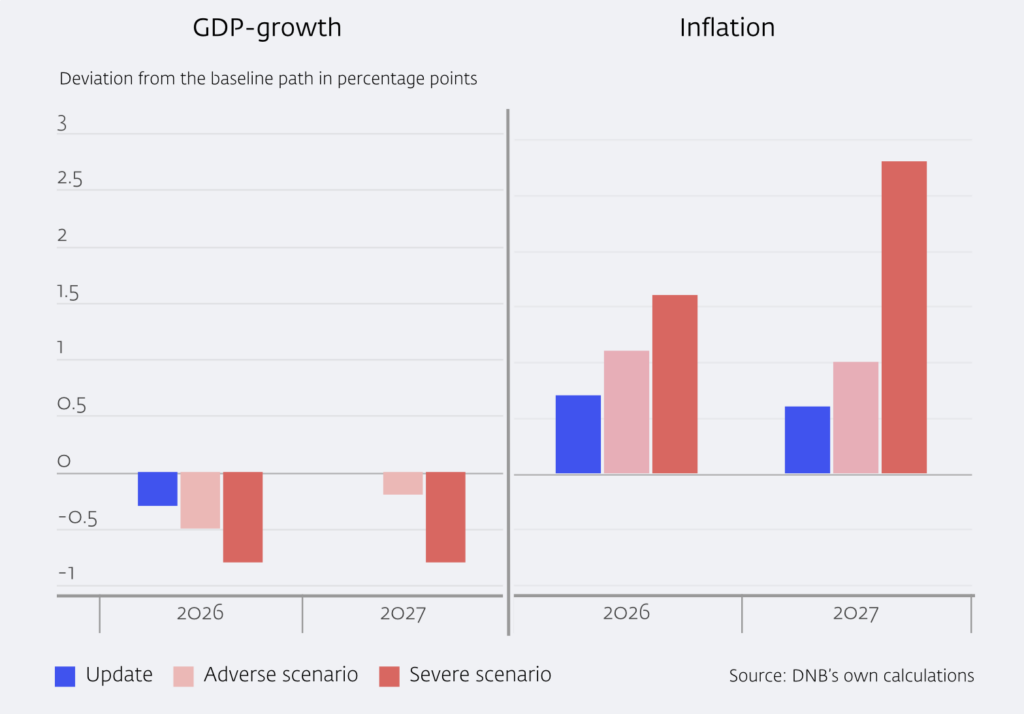

The bottom line is that the duration of the conflict dictates the extent to which the Netherlands and other European countries will suffer economically. Based on DNB’s own calculations, the current worst-case scenario will affect disposable income less than in 2022, but it will affect long-term inflation.

How the Netherlands is impacted and exposed

Even if the conflict is far from Dutch borders, it’s still impacting the economy. Lower-than-expected temperatures have already left the region more exposed, as stocks have been depleted more than usual.

With gas prices benchmarked at €52-€60 and new potential increases, the government is likely to absorb these new prices. While the effects on the economy won’t affect them immediately, they can linger.

Another reason is the AEX structure. The index is concentrated around major oil and gas stocks. In the last week of March, the AEX closed 0.98% higher despite oil shortages, as projected profits from oil and gas distribution continued to drive growth.

On the flip side, the AEX is also focused on tech stocks like ASML. The longer a conflict continues, the more it will likely affect interest rates. In March, the ECB refrained from lowering interest rates. Jesse Simons, Head of Trading at Yieldfund, emphasized that the FED is stuck on how to address the conflict, without continuing to lower interest rates.

What’s important to note is that the ECB emphasized it could raise interest rates, with the market projecting two or even three rate hikes this year. Why is this important? Higher interest rates shift the dynamic to a more cautious one, putting immediate pressure on household budgets.

As purchasing power drops, workers demand higher wages to compensate. This cycle creates wage pressure, leading to second-round inflation effects that are notoriously difficult for central banks to manage. This results in even higher interest rates.

Impact on inflation

Inflation in the Netherlands currently stands at 2.4%, driven by a surge in service-sector prices. While this baseline seems manageable, according to DNB, the figures could rise rapidly if the Middle East conflict continues. Recent reports from De Nederlandsche Bank (DNB) and Rabobank model several risk scenarios.

The worst-case forecast, in which the conflict continues and leads to sustained high energy prices, could push Dutch inflation into the 3.5% to 4.4% range. It’s worth understanding that the same adverse effects will apply to the rest of Europe.

The baseline inflation before the conflict was 3%, in line with European averages; however, analysts warn that a negative scenario could lead to slower economic growth of 0.6% in 2026, compared to the projected 1.5% before the conflict.

Looking at data, consumers are already feeling the pressure at the petrol pump, with fuel pricing climbing past €2.32 per liter. In response, both EU and Dutch policymakers are considering targeted financial support to protect vulnerable households from severe price shocks.

AEX performance In March

In the short term, the oil shock provided a massive boost to the broader European energy sector. The Stoxx 600 energy index rose by 6%, and prominent energy names within the AEX saw significant gains as investors rotated capital into commodities.

However, the medium-term outlook presents a different picture. A 40% jump in TTF gas prices is severely pressuring corporate profit margins across the manufacturing and industrial sectors. More importantly, rising energy costs fuel inflation fears. For the AEX, the prevailing risk is a stagflation narrative—a combination of stagnant economic growth and high inflation. If this narrative takes hold, the initial index gains could reverse entirely as risk appetite dries up.

Outlook and effects of conflict on the Netherlands

Before the geopolitical escalation, the baseline growth expectation for the Dutch economy was a healthy 1.4% to 2.0% for the coming year. Now, financial institutions are lowering the forecast by 0.3% to 0.5%.

In the Netherlands, domestic growth is linked to excess spending. As consumer confidence gets hit by rising heating and essential costs, discretionary spending isn’t funneled back into the economy. Despite rising inflation, household spending is increasing but still struggling to keep pace with the new costs of living.

In a scenario where oil prices remain between $100 and $120 per barrel, second-round wage hikes become inevitable, forcing businesses to raise prices even further. For regular citizens, any hike in gas and oil prices will affect discretionary spending and capital, creating a burden on the broader economy.

The critical tipping point for investors is the 4% inflation mark. If Dutch and Eurozone inflation exceeds this threshold, the European Central Bank (ECB) will face immense pressure to shift its policy. A return to aggressive interest rate hikes would compress projected growth. In this environment, the AEX faces severe downside risk, as global tech and cyclical stocks typically sell off heavily when growth slows and the cost of capital rises.

Navigating macro risks

While analysts create several scenarios for how the Dutch economy will evolve, everything hinges on the duration of the Iranian conflict. Even more importantly is how markets assess the risks and whether futures prices will continue to increase or will stabilize.

Managing risk and diversifying is one way for investors to potentially protect their capital against regional economic uncertainty. If you want to diversify or invest in volatile markets, Yieldfund is a quantitative trading company that provides above-market returns without having to manually invest.

If you are interested in knowing more, book a time with one of our investment relations managers to understand how Yieldfund can work for your portfolio. Book here