The current economic landscape, both national and international, requires an understanding of multiple data points. The S&P 500 recently crossed the $7,100 threshold, reaching all-time highs and boasting a forward price-to-earnings (P/E) ratio of 21.3x. Simultaneously, persistent inflation, geopolitical conflict in the Middle East, and a massive shift in Federal Reserve leadership threaten to upend traditional monetary policy.

Analyzing Kevin Warsh’s vision for Federal Reserve independence

The nomination of Kevin Warsh for Federal Reserve Chair signals a shift in US monetary policy. During his Senate Banking Committee confirmation hearing, Warsh presented a reform-oriented framework designed to strip the central bank of mission creep and return it to a rigid, data-driven mandate.

He argued that operational independence is a cornerstone of effective monetary policy. Yet, he acknowledged that the executive branch will naturally express preferences regarding base rates.

During this hearing, he insisted that the Fed must isolate its decision-making from political cycles with a core thesis that “inflation is a choice,” placing accountability for price stability on central banks. He emphasized a complete overhaul of the Fed’s tactics, including:

- Strict 2% inflation targeting: Warsh intends to dismantle the flexible average inflation targeting framework adopted in 2020, replacing it with a hard 2% ceiling.

- Interest rate prioritization: The new Fed will utilize the federal funds rate as the primary lever for economic intervention.

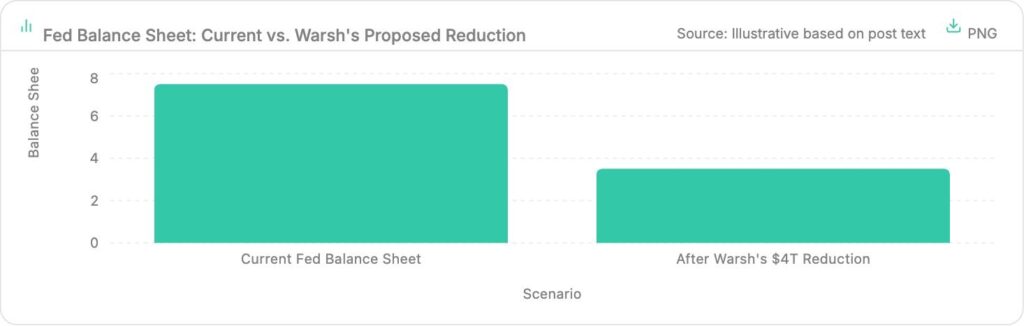

- Aggressive balance sheet reduction: A Warsh-led Fed will actively shrink its asset holdings, pulling back from quantitative easing (QE) to prevent artificial asset inflation.

- Elimination of forward guidance: The central bank will likely abandon the “dot plot,” forcing markets to react to real-time data rather than pre-telegraphed policy projections.

Tracking current market trends and shifting rate cut expectations

Despite looming threats, the market remains highly liquid. In an analysis, 22V Research strategist Dennis DeBusschere emphasizes that a paradox has emerged between immediate market performance and the expected outlook.

The divergence is driven by the “non-QE” liquidity injection, where the Fed bought $40 billion in Treasury bills monthly. It created a huge stimulus, coupled with ongoing fiscal deficit spending, aggressively easing financial conditions.

At the same time, long-term inflation expectations remain artificially anchored, with strong GDP growth between 5-6%. However, Jesse Simons argues that by Warsh seeking to shrink the Fed’s balance sheet by $4 trillion, it will lead to stretched valuations and a fiscal position that’s significantly weaker.

As such, a resilient consumer base spending through supply shocks forces the Fed to maintain, or potentially raise, borrowing costs. Even so, analysts at 22V Research highlight an abnormality with anchored inflation, creating a positive backdrop for stocks to thrive.

Understanding the S&P 500 surge amid ongoing global conflict

Despite a massive oil-supply disruption stemming from the Iran war and the blockade of the Strait of Hormuz, the S&P 500 continues to print all-time highs. And it’s anchored in several behavioral and mathematical drivers.

The market is betting on a rapid de-escalation. A TACO expectation assumes the current administration will pivot to protect domestic growth. Interestingly, even with tensions in the Middle East, earnings season has been positive.

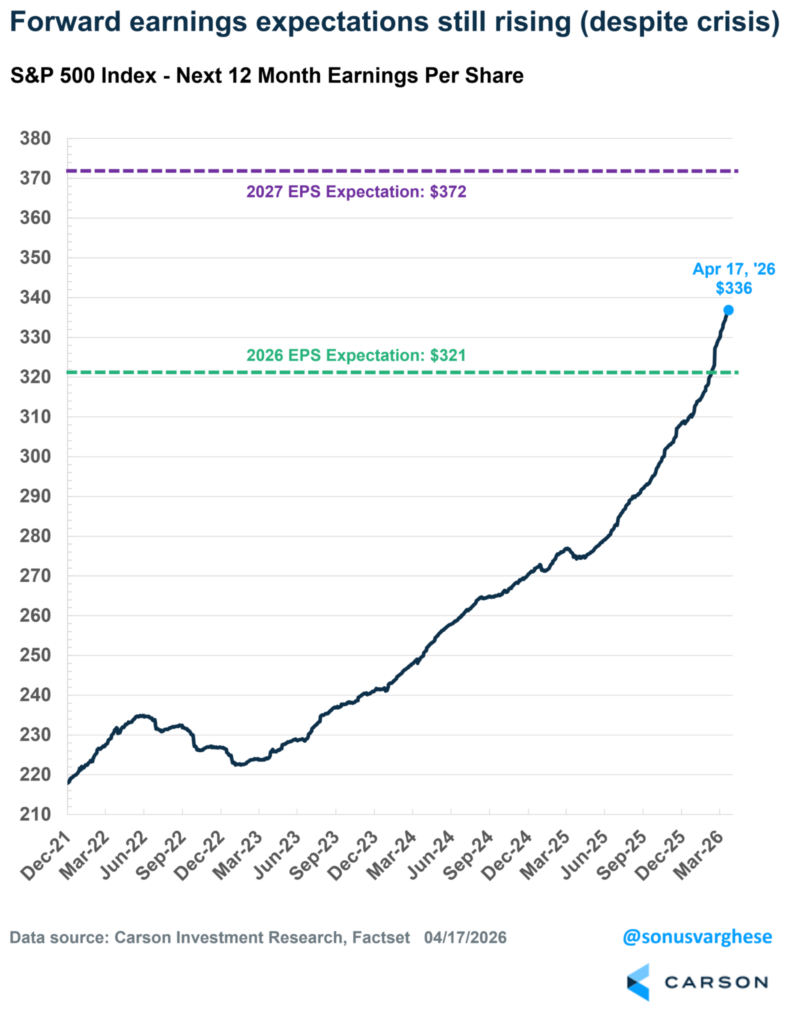

The S&P 500’s year-to-date return is not driven by speculative multiple expansion but by raw profit growth. The index’s next 12-month earnings per share (NTM EPS) has surged to $336. Forward profit margins, which sat at 12% in 2019, have now expanded to a staggering 15.2%. Companies are effectively passing inflationary input costs onto consumers, driving nominal revenues higher.

One of the main growth catalysts is AI, as it is able to deflate geopolitical headwinds. The tech sector, which commands a disproportionate weighting in the S&P 500, is operating on an independent growth cycle. In 2026, AI and stocks could account for over 60% of the total growth as capital expenditure in AI infrastructure translates directly to long-term efficiency. At the same time, the tech sector has seen 2026 EPS expectations grow by 11% and 2027 EPS grow by 15%.

Identifying potential market risks and inflationary dangers for investors

While the data supports current valuations, the horizon is fraught with systemic risks. A profit margin expansion story is inevitably an inflation story, and if input costs outpace consumer purchasing power, the current earnings super-cycle could collapse.

These risks include potential tariff inflation, which, as we’ve seen, is not 100% accurate. At the same time, political announcements can create global uncertainty, and energy market contagion if disruptions in major oil transit routes like the Strait of Hormuz cause crude prices to spike.

Even with self-inflicting wounds caused by tariffs and the ongoing conflicts, the economy is looking to be more resilient than expected. Furthermore, there’s the risk of a Federal Reserve trap; if inflation rebounds, the Fed may be unable to cut rates, leading to surging US Treasury yields that could crush equity multiples.

Diversification for modern investors

To insulate from the potential volatility of the Fed in the coming months, modern portfolios demand cross-asset integration. Along with the S&P 500, the Dutch AEX has reached an all-time high. Even with oil shortages, the Netherlands is able to maintain its position as a major hub for innovation and investing.

If you want to diversify your investments and not only focus on stocks which are subject to macroeconomic effects, Yieldfund provides ways to access crypto yields without the volatility. Yieldfund is a quantitative trading company trading the top cryptocurrencies in the world, offering fixed investment plans and weekly returns—without having investors trade themselves.