Rising bond yields mean governments globally are paying higher interest rates to access capital from investors. This dynamic takes place when bond prices fall due to inflation triggered by geopolitical stress and other factors. Bond yields are the baseline for how the global economy operates and are influencing everything from daily expenses to savings and mortgage rates.

Why are bond yields rising rapidly in 2026

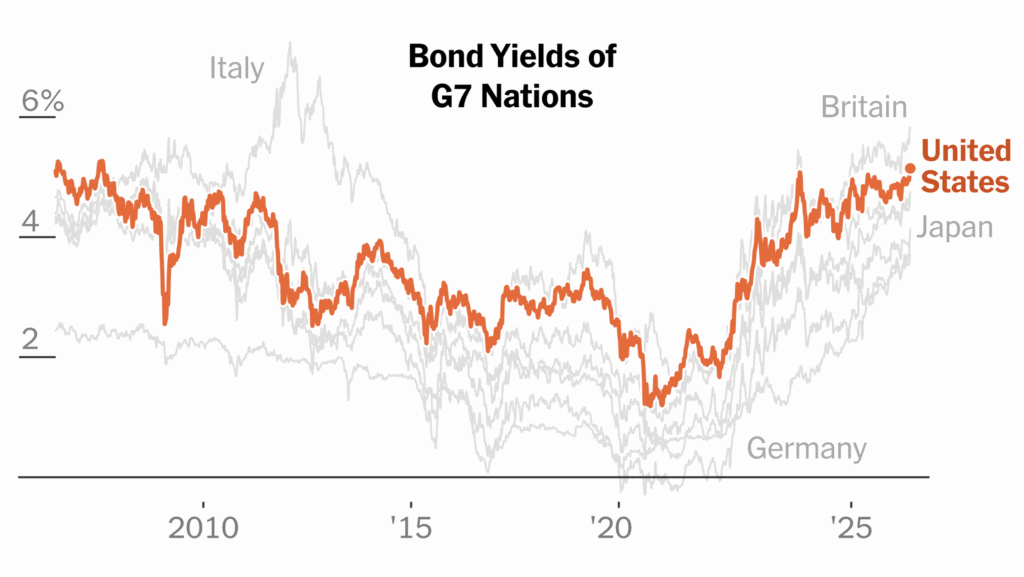

U.S. Treasury bonds have recently reached 5.2%, marking the highest level since 2007, a year prior to the global financial crisis. The surge is driven primarily by geopolitical tensions spiraled by the ongoing Iran conflict as inflation in the US has reached 3.8%, the highest since May 2023.

Bonds have increased rapidly as a response to disrupted energy markets. The CPI index, which tracks purchasing power in the US, rose by 3.8%. Investors now demand higher returns to compensate for growing inflation, which in turn is forcing the government to increase the yields to access capital and reduce risks. The U.S. government’s budget deficit is projected at $1.95 trillion, which means they are required to issue more debt and increase overall supply—pushing yields higher.

What are U.S. Treasury yields and how do they affect growth?

The U.S. Treasury yields are annual returns citizens can make by lending money to the U.S. government. As we described previously, treasury bonds have the same interest as inflation, and in 2026, are expressed as a percent of the bond’s price. For example, earning 4.69% on the 10-year Treasury note.

Treasury yields function as the benchmark for global borrowing costs. When these yields rise, corporations and businesses face higher interest rates on their own loans and limit corporate expansion. In turn, higher bonds have a chain effect and can influence economic growth. Smaller companies tend to devalue when treasury bonds and inflation surge, since they are required to pay more interest on their loans—reducing their profit margins.

How does high inflation push treasury bond yields higher?

High inflation reduces the purchasing power of a bond’s fixed interest payments. For instance, a 3% bond coupon becomes less appealing when inflation is at 4%, as the investor loses money in real terms. Because bond prices and yields have an inverse relationship, rising inflation typically leads to higher yields.

To combat inflation, the Federal Reserve often raises benchmark interest rates. Consequently, newly issued bonds will offer higher rates to attract investors. This makes older bonds with lower payouts less attractive, causing their market prices to fall and their yields to rise. For example, if a bond has a 5% nominal return and inflation is 2%, the real return is only 3%. If inflation climbs higher, the real return diminishes even further, eroding the value for fixed-income investors. This is why investors demand higher yields to justify holding long-term debt when the cost of living is increasing.

Rising yields affecting personal savings accounts

Rising bond yields don’t only move headlines, they also push up the rates banks pay on savings. High-yield savings accounts are pricing off these elevated Treasury levels in the US. In some cases, we’re witnessing APYs of 4% for short-term deposits.

While savings accounts provide higher interest of up to 4% in some cases to align with the current inflation, it’s worth noting that purchasing power will remain the same. Keeping money in savings accounts typically covers the inflation rate. Thus, if banks are paying more, it’s more likely because inflation has also grown higher.

How do bond yields impact mortgage rates and living costs?

10-year Treasury bonds are a benchmark for how much lenders charge for 30-year fixed mortgages. By mid-May 2026, it sits around 4.7%, which feeds directly into higher mortgage pricing. According to data, in the US, the average 30-year fixed mortgage rate has climbed to about 6.75%, up from roughly 6.0% earlier in the year.

What’s important to highlight is that higher yield bonds are increasing mortgage rates. A move from 6.0% to 6.75% can add roughly €160–€170 per month in principal and interest for a €420,000 house. Bonds also transpire into other living costs and credits, which are impacting living costs.

Thus, higher bond yields might only look good in the bank account; however, they are affecting living costs. A 1% increase on a mortgage, 3% on credit, and higher food prices decrease total savings and affect how much people can save and spend—directly affecting the economy. Consumers ultimately bear the brunt of these costs, leading to tighter household budgets.

What is the link between rising bonds and global economic stability?

When U.S. bond yields increase, they are pulling capital away from global stock markets and risk-on investment strategies. That’s because investors can generate more from bonds than from stocks which are less likely to move in a difficult economic context.

Investors naturally flock to the safety and high returns of U.S. government debt, reducing funding for private enterprises and emerging markets. The U.S. Treasury market is a $31 trillion ecosystem that sets the tone for worldwide finance.

In May, the 30-year yields in the United Kingdom approached 6%, while German long-term rates hit levels unseen since 2011. This synchronized global selloff in bond prices pressures central banks to raise their own interest rates. It’s worth noting that if the cycle continues, it can trigger a broader economic slowdown. The ECB has already warned that economic growth will be affected in the shorter and medium terms and heavily indebted countries will struggle to finance their public deficits.

How to protect your portfolio during bond market volatility

In periods of high volatility where bond prices are falling, justifying risk-on strategies becomes more difficult. While bonds are attractive for experienced investors, retail is likely to lose money as they won’t be ahead of most capital rotation.

Yieldfund provides an investment alternative where retail investors don’t have to worry about tracking volatility or portfolio performance. They simply access an investment plan which pays up to 48% yearly returns and receive weekly payouts in USDC directly in their wallet.

Frequently Asked Questions

What causes bond prices to drop when yields go up?

Bond prices and yields have an inverse relationship. When new bonds are issued with higher interest rates to combat inflation, older bonds with lower rates become less desirable.

How long will Treasury yields remain above 5%?

Treasury yields will likely remain elevated as long as inflation stays high and geopolitical conflicts like the Iran war disrupt global energy markets.