Compounding interest is how wealth is built effectively since it lets invested capital snowball into more capital that grows faster the longer someone lets it stay invested. In finance and investing, it’s one of the ways to accumulate wealth without dividends.

- Compounding interest means earning returns on the main invested amount as well as the accumulated returns.

- Wealth builds over time, and investing earlier can add more to a retirement balance than starting later.

- Fees and taxes are hidden expenses retail investors fail to account for when calculating their expected total returns.

What is compounding interest in finance?

Compounding interest is the interest people earn on the initial investment but also on the returns they received from their investment. Explained simply, it’s the interest someone earns on their existing earned interest.

Compounding works since any interest that is generated by an investment is added back into the main principal. This makes the total invested capital higher, and earning the same interest on a higher investment yields higher interest per year or month.

With compound interest, the invested balance grows at an accelerating rate because each period’s earnings are added to the base that generates the next period’s earnings.

Consider a €5,000 investment earning 10% annually. In year one, you earn €500, bringing your balance to €5,500. In year two, you earn 10% not just on the original €5,000 but also on that €500. Putting it in perspective, a €5,000 investment can grow to approximately €100,000 in 30 years.

How compounding works for everyday investors

Compounding works when investment returns are added back into the investment account rather than withdrawn. Every euro or dollar you reinvest gets added to the main invested account, which grows the total invested capital and indirectly the returns for the next month.

When you invest in the stock market, ETFs, or crypto, you don’t earn a fixed interest rate. In our experience, the returns which are generated are the result of the changing value of your investments. In some cases, the stock market also pays out dividends.

For retail investors, when those returns stay invested rather than withdrawn, that’s when compounding takes place. On quantitative trading companies like Yieldfund, investment plans pay out weekly. Investors don’t add the money back into the plan, so they are not compounding their wins.

Why focus on compounding vs. simple interest?

Compound interest matters more than simple interest because the gap between them widens dramatically over time. Early on, the difference is small. Over decades, it becomes enormous.

Using an example of a starting balance of a €6,000 balance at a 3.5% rate, here’s how both interest types stand out:

| Time period | Simple interest balance | Compound interest balance |

| Year 1 | €6,210 | €6,210 |

| Year 10 | €8,100 | €8,464 |

| Year 30 | ~€12,300 | ~€16,840 |

After 30 years of investing, compounding interest adds more capital to someone’s balance. Based on the calculation, it adds another €4,500 on the same starting balance without extra effort. When people look to invest for retirement, compounding interest is more recommended because capital is stacking and you don’t lose interest opportunities.

When comparing investment options, look beyond the headline rate. An account that compounds will always outperform one that pays simple interest at the same rate, or that pays dividents.

How is compounding ROI calculated?

Calculating compounding interest takes into consideration the main investment (the principal), the rate of return or percentage increase, and how frequently those returns are reinvested.

From our view, understanding how often your interest is added back into the principal means you’re able to earn a lot more from your investments. For example, when returns are added every year, your investment is losing opportunities to earn more. Weekly or monthly contributions might not seem like a big difference, but they make up for higher returns over a longer period.

For a quick estimate, you can use the Rule of 72. This simple trick helps you approximate how long it will take for your investment to double. Just divide 72 by your annual rate of return. The S&P 500 has historically provided up to 8% returns.

Strategies to maximize compounding interest

To maximize the effects of compounding, there are a few things that can be done by any type of investor. That’s because they create a pattern and a foundation for compounding capital to grow faster and have a bigger impact on the total capital. These strategies include:

Investing early

The most valuable fuel for a compounding strategy is time, because it allows for interest to add up and grow the principal amount. One year’s difference isn’t creating such a big difference, but starting 5 or 10 years earlier can add thousands more.

The upside is that investing early means a lower investment can grow to the same amount as someone who invests €100,000. Investing €6,000 per year at 7% until the age of retirement can have different outcomes. Someone who starts at 25 retires with approximately €1.5 million, while someone who starts at 30 ends up with €1 million. That’s €500,000 less despite investing only €30,000 less.

Invest often

Regular contributions feed the compounding engine and can reduce risk. Steady investing and DCAing through both market highs and lows means you buy the same amount at the same time regardless if it’s higher or lower.

This not only helps keep investing structured, but it helps retail investors remove emotions from trading. Investing often and having weekly or monthly compounding creates faster ways to grow an investment portfolio.

How is compounding calculated in finance?

Compounding interest is calculated by applying the return rate to a balance that includes all previously earned returns, repeated over each compounding period. The more frequently it compounds, the faster the balance grows. The compounding frequency varies by product: savings and money market accounts typically compound daily, while certificates of deposit (CDs) compound daily or monthly.

Bonds compound semi-annually, loans often compound monthly, and credit cards compound daily, which is why card debt grows so quickly. For building wealth through compounding, the idea is to have a higher number of compounding periods which translate to greater compounding interest.

Why isn’t every investment compounding?

Not every investment is compounding automatically, because some are paid out rather than reinvested. For example, most company stocks pay out dividends to their investors and if they are not added back as a stock, they won’t yield higher returns.

There is a difference between compounding and non-compounding investments and the reasons depend on the type of investment you’re choosing. Some investment tools like ETFs have dividends and accumulation. Dividends are paid out yearly based on the fund’s performance, while accumulation is accumulating/compounding the returns.

Reinvestment is central to building wealth. The key difference between compounding and non-compounding investments lies in how returns are handled. When earnings are withdrawn from the investment, they can no longer generate further growth, so for an investment to compound, earnings must be reinvested, either automatically or manually.

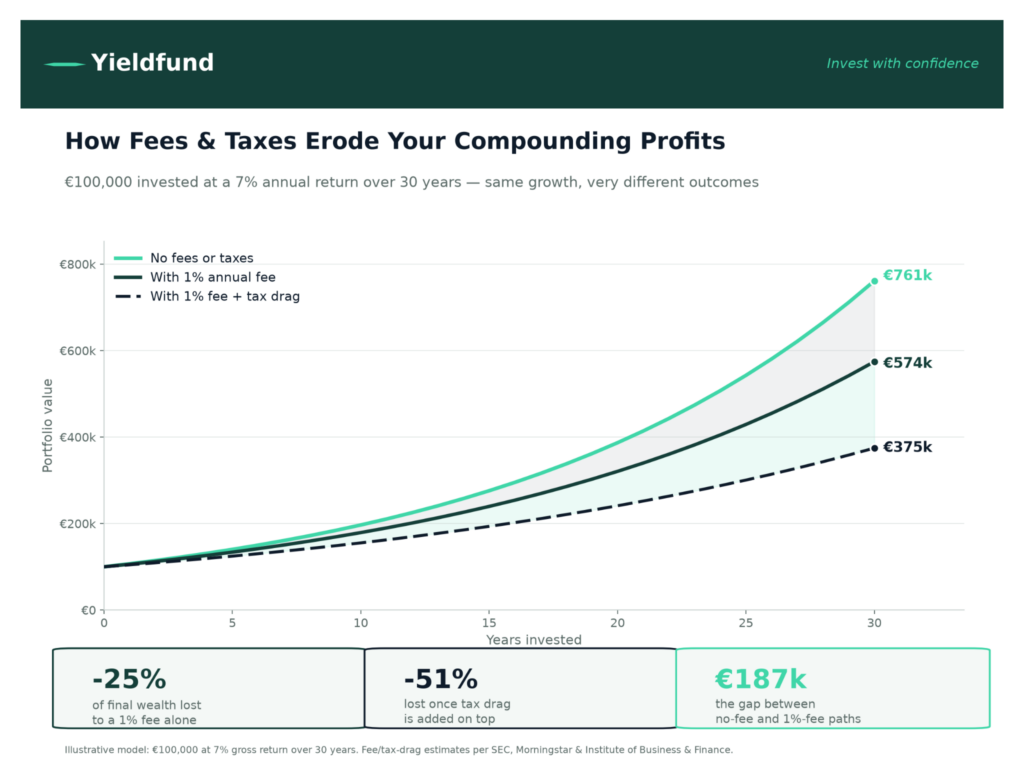

How fees and taxes affect your net compounding interest profits

Although compounding can significantly increase an investor’s wealth, the often-cited 7% average annual return from the S&P 500 isn’t what investors actually keep. Capital gains taxes, levied when an investment is sold, can reduce this final amount.

While fees and taxes may seem like a small percentage, they compound against you over time. Every euro paid in fees or taxes is a euro that no longer earns future returns.

Consider an investment with a 7% annual return. A fund charging just a 1% annual fee could reduce your final balance by roughly a quarter over 30 years. For example, a portfolio that should have grown to €761,000 would instead be closer to €574,000, with more than a 15% loss.

Taxes have a similar effect. Paying tax on gains annually in a regular account, rather than letting them compound untouched, can reduce your final wealth by 25–40% over several decades. Fortunately, this is one part of compounding you can control.

By choosing low-cost index funds and using tax-advantaged accounts where returns grow uninterrupted, you can ensure the math of compounding works for you, not against you.

Final words

For investors, compounding interest rewards is about creating a structured plan and acting on it early. Investing regularly, starting as early as possible even with a lower budget, has the potential to turn modest contributions into substantial portfolio wealth over time.

A first step for retail investors is to know how compounding is calculated, what returns to look for, and weigh them against unknown future fees. Accumulating stocks adds compounding without extra work, while other financial instruments like quantitative trading companies such as Yieldfund pay out weekly, and the payouts have to be reinvested to compound.

Frequently asked questions

What is compound interest in simple terms?

Compound interest means earning returns on both your original money and the returns it has already earned.

How long does it take compound interest to make a real difference?

Compounding works gradually, with the biggest gains starting to appear over 10 or 15 years.

Does compounding frequency really matter?

Yes, the more often interest compounds, the faster your balance grows since reinvesting money every one year compared to every month makes a significant difference.

What’s the difference between compound interest and compound returns?

Compound interest applies to savings accounts, bonds, and loans. Compound returns is a broader concept that includes dividends and capital gains from stocks, mutual funds, and other investments.