The difference in risk between bank interest and Yieldfund is that banks protect capital up to €100,000 per person per account and are lower risk as some see it. Yieldfund returns come from the quantitative trading algorithm that trades the crypto market and pays investors based on their investment plan.

For investors, the distinction has to be “what risk they are accepting in exchange for the level of returns”. To keep the article transparent, this is not financial advice.

What is bank interest

Interest from banks is the return banks are paying their customers for using their services. This includes deposits and savings accounts. What bank customers don’t know is how the money is used by the banks to generate returns for themselves. Banks use customer deposits as part of broader lending and liquidity operations.

One of the main advantages of banks is they are more regulated and are part of the Dutch Deposit Guarantee. It protects eligible money in Dutch bank accounts up to €100,000 in case the bank goes bankrupt.

Retail investors who use banks to increase their wealth are making a tradeoff. Interest is usually modest, which is designed for safety instead of building capital.

Why is bank interest considered lower risk

Banks are seen by investors to be lower risk because they are covered nationally and are designed to keep funds as secure as possible. De Nederlandsche Bank administers the Dutch Deposit Guarantee on behalf of the government and protects eligible deposits up to €100,000 per person, per bank.

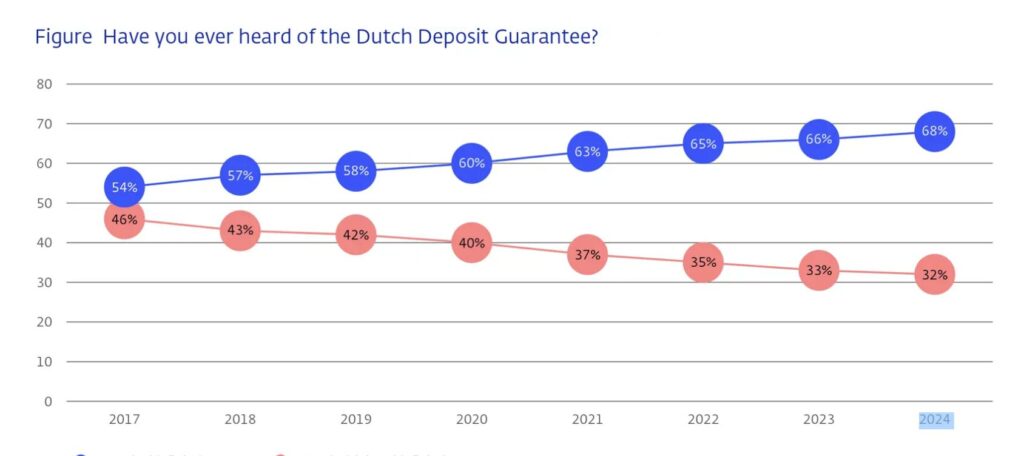

What many retail investors don’t understand is that even if risk levels are low, there are still risks. Recent data shows that awareness of the Dutch Deposit Guarantee has increased to 68% according to the DNB.

Regardless, banks can still fail, interest rates can change, and inflation can reduce the real value of money. According to Dutch bank rates, ABN AMRO has shown saving rates of 1.25%, while the DNB has shown deposit interest ranges over the years—from a low of 0.88% in May 2021 to 4.86% in October 2008, depending on macroeconomic events.

Even so, deposit protection is the same, regardless of the interest rates, which is why bank savings are seen as safer than private investment products.

Why does Yieldfund carry a different type of risk

Yieldfund carries a different type of risk compared to banks because it depends on the fund’s performance. Yieldfund is notified with the AFM but does not participate in the deposit guarantee scheme; however, the returns Yieldfund provides are above bank averages.

Yieldfund is a quantitative trading company. It relies on trading algorithms to generate returns and pay out fixed terms based on the investment plan (between 24% – 48% per year). Another difference is that Yieldfund trades the crypto markets and is transparent about the type of software trades they are performing.

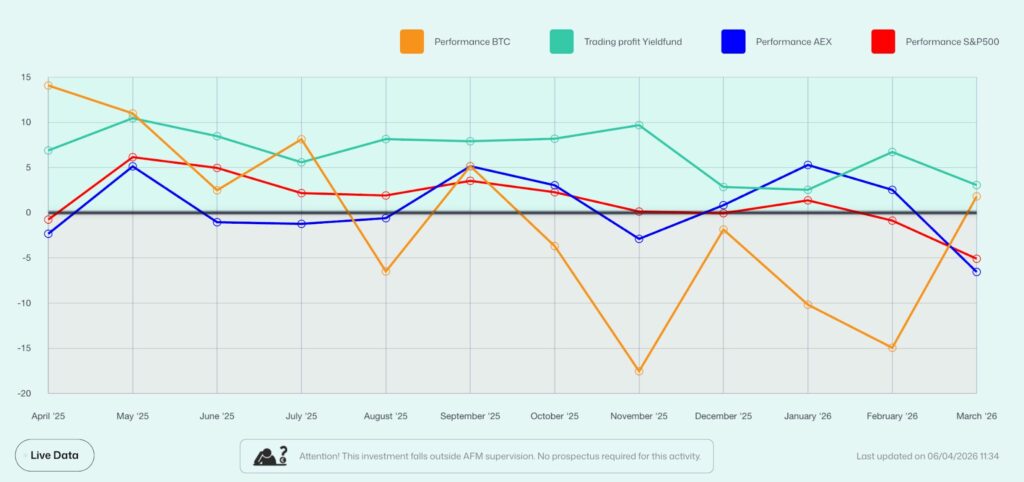

For regular investors who are unfamiliar with alternative investments, the risk can be higher as they have a lower risk tolerance. The upside with Yieldfund is that they pay out a much higher yield compared to banks, while trades and investments are visible through the performance page. It generated +124.8% net yearly profit in 2025 and has outperformed the S&P 500 and the AEX 11 out of the 12 months.

Bank interest vs Yieldfund: what is the key risk

The key risk difference is that bank interest protects capital first, while Yieldfund aims to generate higher investment returns through trading. A bank savings account is built around security, liquidity, and deposit protection, while Yieldfund is built around structured access to trading-based returns.

This creates a clear trade-off for investors. Banks usually offer lower returns with stronger legal protection, while Yieldfund offers higher potential income with higher product, company, and market risk.

A simple way to compare them is this:

| Factor | Bank interest | Yieldfund |

| Return type | Savings interest | Fixed-interest investment plan |

| Main source of return | Bank deposit model | Quantitative crypto trading |

| Return level | Usually lower | Higher, depending on plan |

| Risk level | Lower | Higher |

| Liquidity | Usually easier access, depending on account type | Interest paid out weekly |

| Best suited for | Capital preservation | Investors accepting more risk for higher returns |

What are investors actually choosing between

Investors are choosing between security and return potential. Bank savings are usually better suited for emergency funds, short-term reserves, and money that should not be exposed to investment risk.

Yieldfund is better understood as an investment product, not a replacement for a protected savings account. It may suit investors who want higher weekly income potential and are comfortable accepting the risks that come with a private, trading-based structure.

That distinction matters because both products can have a place in a broader financial plan. A cautious investor may keep essential cash in a bank account and only allocate risk capital to products like Yieldfund.

Is Yieldfund riskier than getting interest from a bank

Yieldfund carries a higher risk than banks, but what investors need to understand is that there is no such thing as a risk-free investment. Bank deposits can fall under the legal guarantee scheme, but a deposit of €200,000 will still lose €100,000 if the bank fails. With banks, investors are only protected up to €100,000, which is an important distinction to make.

Yieldfund returns depend on the company’s investment model, trading performance, and internal risk controls. That does not automatically make Yieldfund unsuitable. It means investors should evaluate their risk profile and whether they are looking to build wealth and take risks or only save.

The higher return is part of the risk-reward trade-off. When an investment offers materially higher returns than a bank account, investors should also expect a materially different risk profile.

What should investors check before comparing bank interest with Yieldfund?

Before comparing bank vs. Yieldfund risks, they should look for how risk is managed, the return source, and potential downside risks. These details matter more than the headline return.

The most useful questions are:

- Is my money covered by a legal deposit guarantee?

- What is the source of the return?

- How often are payouts made?

- Can I access my capital within a reasonable time?

- What happens if market conditions change?

- What internal risk controls are in place?

- How are funds used by the companies/banks?

Key takeaways: bank interest is lower-risk, Yieldfund has higher return potential

Bank interest is lower-risk compared to Yieldfund, but the returns are only suitable for saving and not building wealth. Yieldfund has higher return potential, but it also carries higher investment risk because returns are linked to the quantitative trading model.

The practical takeaway is simple. Use bank accounts to save money and look to Yieldfund and other alternative investment companies to build wealth if you are comfortable with taking on more risk.

FAQ

Is Yieldfund the same as a bank savings account?

No, Yieldfund is not the same as a bank savings account. A bank account pays deposit interest, while Yieldfund offers fixed-interest investment plans linked to quantitative crypto trading.

Is bank interest risk-free?

No, bank interest is not completely risk-free, but eligible deposits in the Netherlands are protected up to €100,000 per person, per bank, under the Dutch Deposit Guarantee.

Why does Yieldfund offer higher returns than banks?

Yieldfund offers higher returns because it is based on a trading-driven investment model rather than a traditional savings model.

Should investors compare Yieldfund directly with a savings account?

Investors should compare Yieldfund and savings accounts by risk first, not just by return. A savings account is mainly for capital safety, while Yieldfund is an investment product for higher returns and wealth building. oil shortages, the Netherlands is able to maintain its position as a major hub for innovation and investing.