The 50-30-20 rule is a simple budgeting method that divides your monthly net income into three categories: 50% for basic needs, 30% for wants, and 20% for saving and investing. This formula gives you a clear framework to manage your finances and build long-term wealth without overcomplicating your daily life.

What is the 50-30-20 rule

The 50-30-20 rule is a financial framework that allocates 50% of your after-tax income to basic needs, 30% to personal wants, and 20% to savings or debt repayment. It simplifies money management by using broad percentage categories instead of granular line items.

For a Dutch resident earning an average net income of €2,300 per month, this means €1,150 goes to fixed costs, €690 to lifestyle choices, and €460 to investments or savings. By regularly keeping your expenses balanced across these main spending areas, you can put your money to work more efficiently and build wealth over time.

Where did the 50-30-20 rule appear

The 50-30-20 rule originates from the 2005 book “All Your Worth: The Ultimate Lifetime Money Plan,” authored by US Senator Elizabeth Warren and Amelia Warren Tyagi.

They determined that balancing spending across three main categories provides enough structure to prevent debt while allowing for personal enjoyment. Today, the same framework is being implemented by fintech companies to provide options for regular people to maximize the effectiveness of their investment.

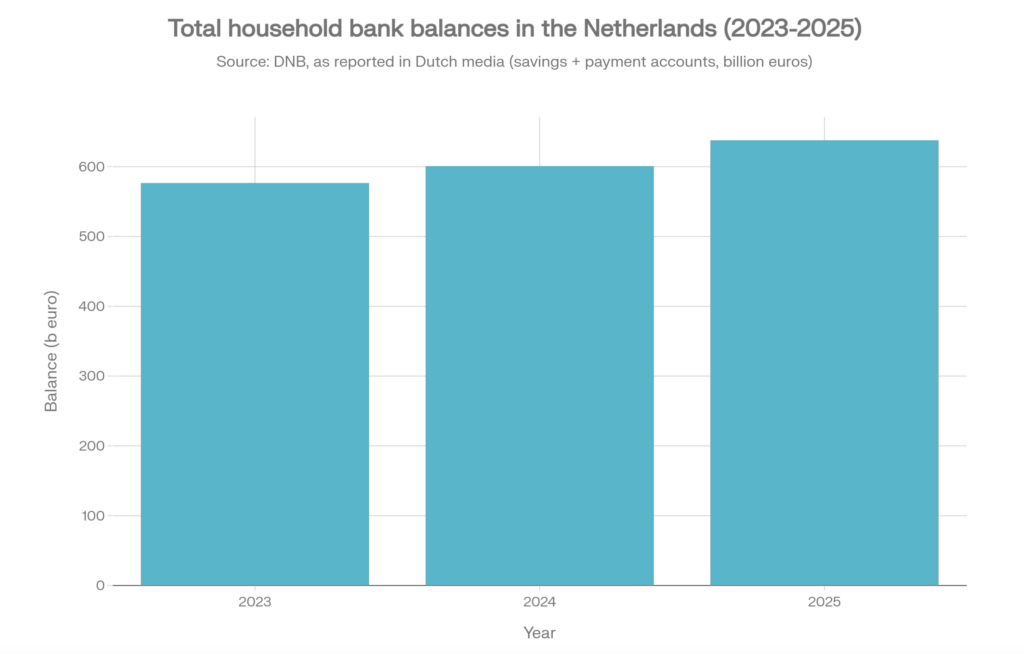

How much are people saving in the Netherlands

Dutch households consistently demonstrate strong saving habits, but actual amounts vary. In 2024, the DNB showed that Dutch savings amounted to €444.4 billion, with an average of €54,700 per household. By the end of 2025, savings accounts in the Netherlands reached €637.6 billion.

Eurostat data shows Dutch households are aligned with the 50-30-20 rule. According to the data, 17.42% of disposable income was saved on average, which is above the European mean of 14.44%.

How to manage your monthly budget with 50-30-20

Managing your monthly budget requires calculating your net income and dividing it strictly into three distinct spending buckets. You must evaluate your past 30 days of bank statements to see exactly where your money currently goes. Subtracting taxes and business expenses (if you are a freelancer) gives you the baseline number to apply your 50%, 30%, and 20% calculations.

50% on basic needs

Basic needs encompass all fixed, unavoidable expenses required for your survival and legal compliance. These are the costs you must pay regardless of your lifestyle choices. In the Netherlands, this category heavily features rent or mortgage payments, mandatory basic health insurance (basisverzekering), groceries, utilities, and transportation. If your needs exceed 50% of your income, you must explore structural life changes, such as switching energy providers or finding a more affordable living situation.

30% on wants

Wants cover the non-essential expenses that make your life enjoyable and comfortable. These items improve your quality of life but can be eliminated if you face a financial emergency. Typical examples include dining out, gym memberships, streaming subscriptions, vacations, and hobbies. Keeping these discretionary expenses capped at 30% ensures you enjoy your current lifestyle without sabotaging your future financial goals.

20% on investing

The remaining 20% focuses entirely on securing your financial future through saving, investing, and debt reduction. This allocation builds your net worth over time. You should prioritize paying off high-interest debt first, then establish an emergency fund, and finally direct capital toward investments like index funds or managed portfolios to harness compound interest.

Guide on how to maximize your 50-30-20 money plan

Maximizing this budget involves automating your cash flow and regularly auditing your expenses. You can instruct your bank to automatically transfer 20% of your salary into a separate investment or savings account the moment you get paid. This strategy removes the temptation to spend your investment capital.

Additionally, reducing expenses in your “needs” category—such as switching energy providers or finding cheaper health insurance during the open enrollment period—frees up more capital. You can then redirect this extra money into your investment portfolio to accelerate your wealth building.

What is the difference between 50-30-20 vs Zero-Based Budgeting

Zero-Based Budgeting assigns a specific job to every single euro until your monthly income minus expenses equals exactly zero, whereas the 50-30-20 rule uses broad percentage buckets. Zero-based budgets provide highly detailed tracking and strict control over spending.

The 50-30-20 method offers simplicity and flexibility, making it much easier to maintain for cautious retail investors who find granular tracking overwhelming. You can even combine both methods by using the 50-30-20 rule for overall structure and zero-based budgeting for specific problem areas.

How to hierarchically invest your 20%

Investing 20% of your salary or monthly budget has to be structured to minimize potential future losses. That’s why allocation has to be made based on the level of risk and potential performance.

When you save 20%, it’s important to avoid having any debt. Typical debt such as credit cards or loans comes with interest (10% on average). Secondly, people should save 3 months’ worth of salary in case of an emergency.

Only once the basics are covered should allocations take place. Investment options can include government bonds, high-yield bank deposits, the stock market which is riskier, or crypto investing. Yieldfund provides a way to invest in crypto without prior knowledge and pays out in structured bonds based on the chosen plan.

Start budgeting for your future

Following the 50-30-20 rule is a simple way to approach your salary and manage your budget more effectively. With inflation creeping into the Dutch economy, saving is becoming increasingly important.

If you already follow the rule or are just getting started, Yieldfund is an alternative way of investing through a structured approach. With Yieldfund, investors can generate up to 48% yearly returns depending on the chosen plan and receive weekly payouts to their crypto wallets.

FAQ

Can you automate the 50-30-20 savings rule?

In our past experience, the 50-30-20 rule can be automated with budgeting applications or by using modern banks. You simply set up automatic standing orders to move 20% of your incoming salary to an investment account.

Which Dutch banks offer tools to help manage finances with the 50-30-20 rule?

Most major Dutch banks and modern financial technology companies like Bunq, ING, and N26 provide automatic routing or everyday round-ups to make saving the 20% easier.

How to categorize expenses accurately using the 50-30-20 method?

Categorizing expenses accurately requires asking yourself if you could physically survive without the item. If you can live without it, the expense belongs in the 30% “wants” category rather than the 50% “needs” category. Reviewing your bank statements monthly ensures you maintain accurate classifications and adjust your spending behaviors accordingly.