Lifestyle inflation means that as your income rises, your spending rises with it, so your financial position does not improve as much as you expected. In the Netherlands in spring 2026, that risk is especially relevant because wages are rising again, while inflation, weak household sentiment, and higher living costs still make it easy for extra income to disappear before it becomes savings or invested capital.

What is lifestyle inflation, and how does it impact investors

Lifestyle inflation occurs when higher income leads to higher spending rather than higher wealth. It usually happens gradually through better housing, more convenient spending, more subscriptions, more travel, and a higher monthly baseline that starts to feel normal.

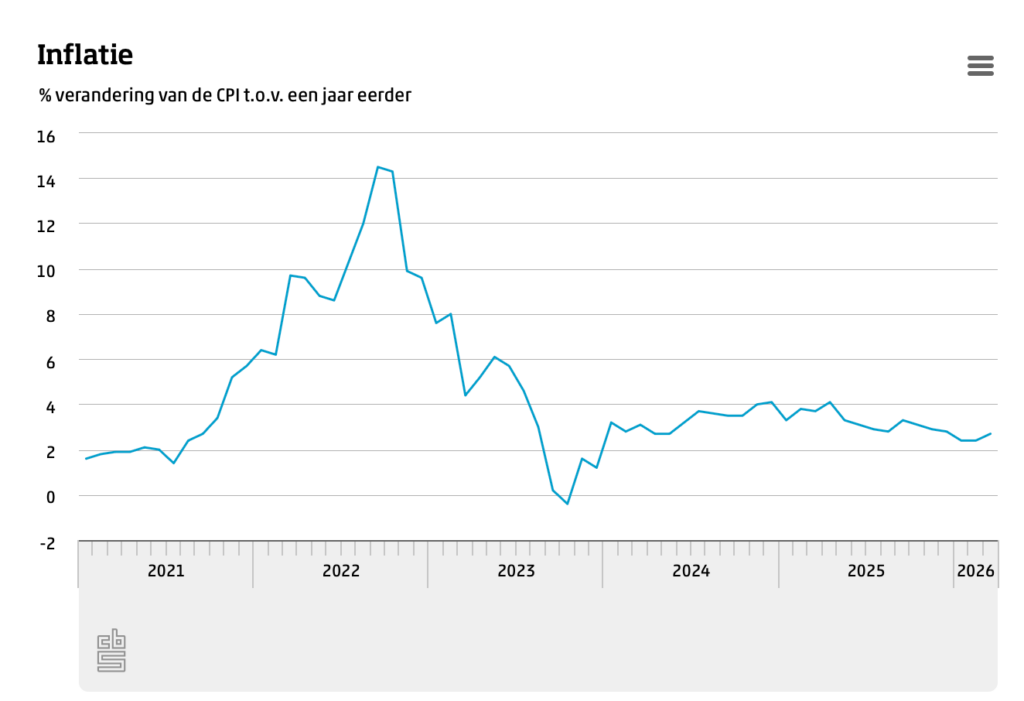

Dutch data shows the tension between inflation and wages. CBS reported that inflation rose from 2.4% in February to 2.7% in March 2026, while negotiated wages in Q1 2026 were 4.5% higher year on year and 2.0% higher in real terms after inflation.

Similarly, household consumption in the Netherlands fell by 0.5% in February. This suggests that higher wages do not automatically translate into higher purchasing power, which affects people’s lifestyle.

The basis of the analysis is that over 60% of U.S. citizens are unable to sustain their current lifestyle and are living paycheck to paycheck, according to research by LendingClub. As such, households in the US aren’t able to sustain their lifestyle and even build wealth as they are unable to save.

In the Netherlands, this matters because, as data shows, lifestyle inflation differs from standard inflation.

This matters because income growth only builds wealth when a portion of it is invested. If every raise, bonus, or business gain is absorbed into day-to-day life, then earnings improve on paper while your long-term capital base barely changes. Lifestyle inflation is when your own spending rises because your habits, standards, or fixed costs rise.

That distinction is important in 2026 because Dutch households are dealing with both at once. CBS said consumer prices in March were 2.7% higher than a year earlier, which means even unchanged spending already costs more.

Why is lifestyle inflation a risk for Dutch investors right now

Lifestyle inflation prevails because Dutch wagers are improving. At the same time, these households still don’t appear to be confident in increasing their spending. CBD data shows that negotiated wages rose by 4.5% in Q1 of 2026, while real wage growth only came to 2.0% after inflation.

For regular investors, this isn’t a confident outlook since a positive increase doesn’t equate to higher capital to be invested. The broader data still points to caution as household consumption volume fell 0.5% in February 2026 after a 0.3% decline in January, which suggests consumers are not acting like they feel flush with cash.

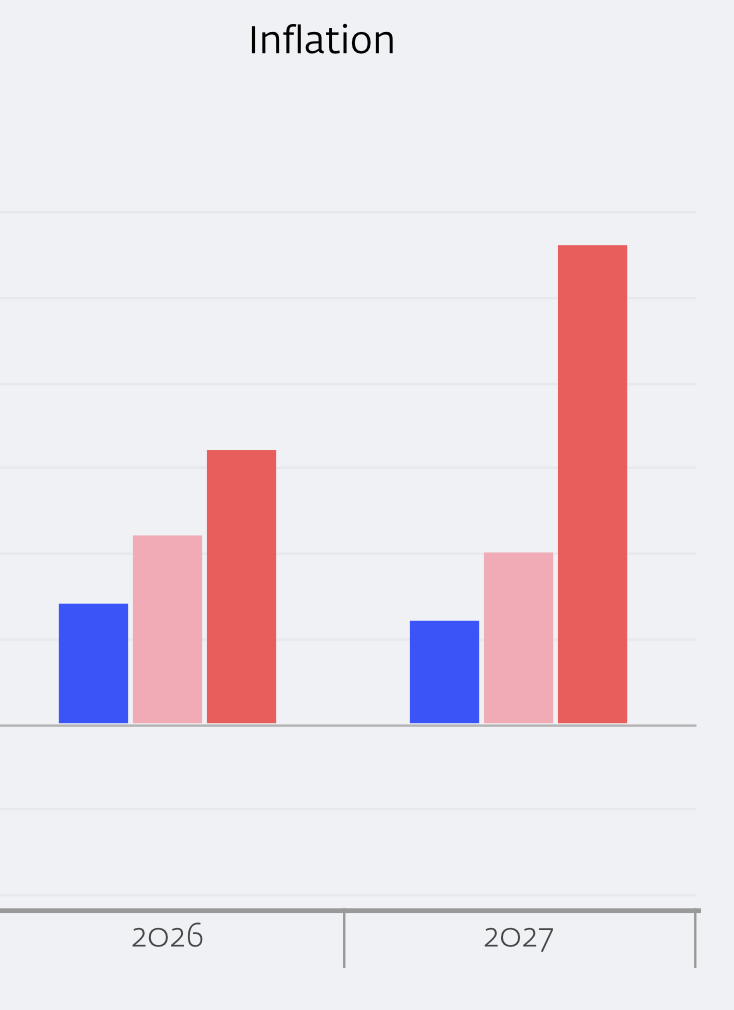

DNB emphasized on March 24th, following the Middle Eastern conflict, that higher energy prices could raise inflation by more than half a percentage point in both 2026 and 2027. They reiterated that energy supply shocks will lift inflation while weakening growth.

A scenario proposed by the DNB shows that in the worst context of the Middle Eastern conflict, Dutch households should expect slower growth and much higher inflation. The scenario points to increased inflation by 1.6% in 2026 and by 2.8% in 2027

Thus, if income rises in a period where prices, uncertainty, and fixed costs stay elevated, then more earnings can easily turn into more spending instead of more capital.

Where does lifestyle inflation show up in real life

In real life, lifestyle inflation usually shows up first in recurring costs rather than one-off purchases. That is why it often feels harmless at first but becomes expensive over time.

Housing is the clearest Dutch example. CBS reported that prices of existing owner-occupied homes in February 2026 were 5.4% higher than a year earlier, which means a move into more expensive housing can absorb income gains very quickly.

A more expensive mortgage or rent level does not just raise one monthly bill; it lowers the amount left for savings, investing, and financial flexibility every month after that.

Convenience spending is another common source of lifestyle inflation. More delivery, more dining out, more digital subscriptions, more travel, and higher recurring service use can all feel manageable individually, but together they raise the household’s default spending level.

Why does lifestyle inflation matter for wealth building

For retail and even investors, lifestyle inflation matters because it slows capital formation even when income is improving. The hidden risks for regular people are that lifestyle inflation isn’t as sudden as regular inflation, and wage data can often be misleading.

Real wages in the Netherlands are up, but inflation is still positive, resulting in a weakening of consumption. At the same time, the Dutch central bank is still warning about renewed price pressure points. Thus, households that want to save and not live paycheck to paycheck don’t have unlimited room to spend.

A better benchmark isn’t salary growth alone. The better benchmark is investable surplus, which means the amount left after essential costs and planned spending that can actually be put to work in the market.

In contrast to the US households, Dutch households are better positioned due to the acceptable cost of living as well as the higher media salaries. Nonetheless, the goal is not to avoid higher income, but to ensure income growth also generates a measurable gap between expenses and income.