So, what creates better cash flow: bank interest, dividend stocks, or structured investing? The short answer is that each works best for a different job. Bank interest is the most stable and liquid option, but the income is usually modest after inflation. Dividend stocks can offer higher long-term income potential, but payments and share prices move with the market. Structured investing like Yieldfund can be used to design a more intentional cash-flow profile.

For Dutch investors, this comparison matters because cash balances are high, inflation has reduced purchasing power, and traditional savings rates may not be enough for investors who want recurring income. This article compares bank interest vs dividend stocks vs structured investing using Netherlands and EU data, then explains where Yieldfund-style structured investing can fit inside a broader cash-flow portfolio.

Why cash flow matters more than yields

Cash flow is one of the most practical goals in investing. It pays bills, supports retirement planning, and gives investors the feeling that their capital is working. But the question is not simply which product has the highest advertised yield. The better question is: which source of cash flow is reliable, repeatable, and appropriate for the risk being taken?

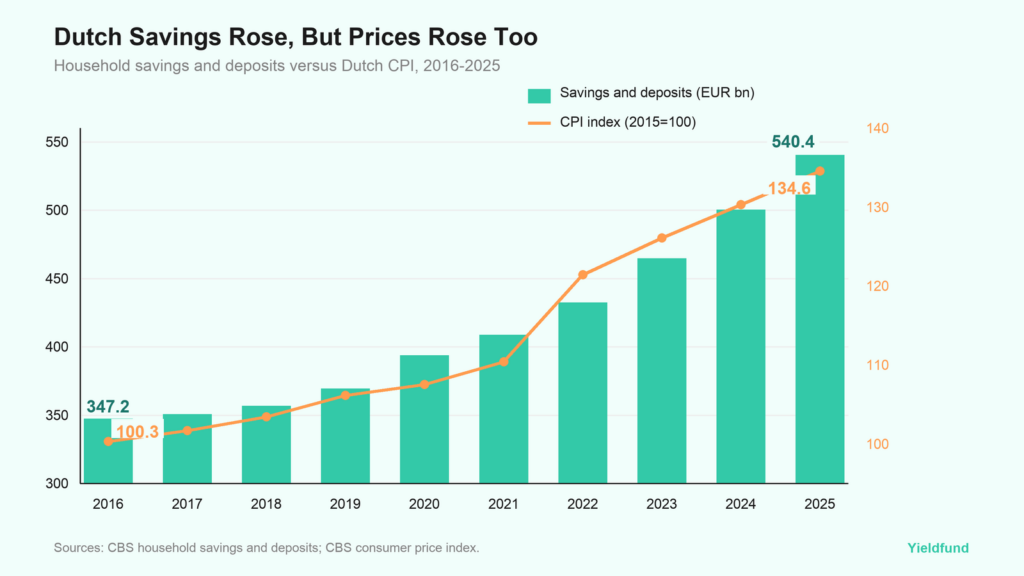

That matters especially in the Netherlands, where households are holding a very large amount of money in cash-like products. Statistics Netherlands reported that Dutch households had more than EUR 540bn in savings and other deposits at the end of 2025. That was up from EUR 347.2bn in 2016.

The problem is that cash balances grew while prices also moved sharply higher. Dutch CPI rose from 100.32 in 2016 to 134.56 in 2025, meaning the general price level increased by roughly 34% over the period. Inflation hit 10.0% in 2022, then remained at 3.8% in 2023, 3.3% in 2024, and 3.3% in 2025.

For investors, this changes the cash-flow conversation. A savings account can pay interest, but if that interest does not keep pace with inflation, the income may feel safe while purchasing power erodes.

Bank interest: Safe, liquid, but often too low

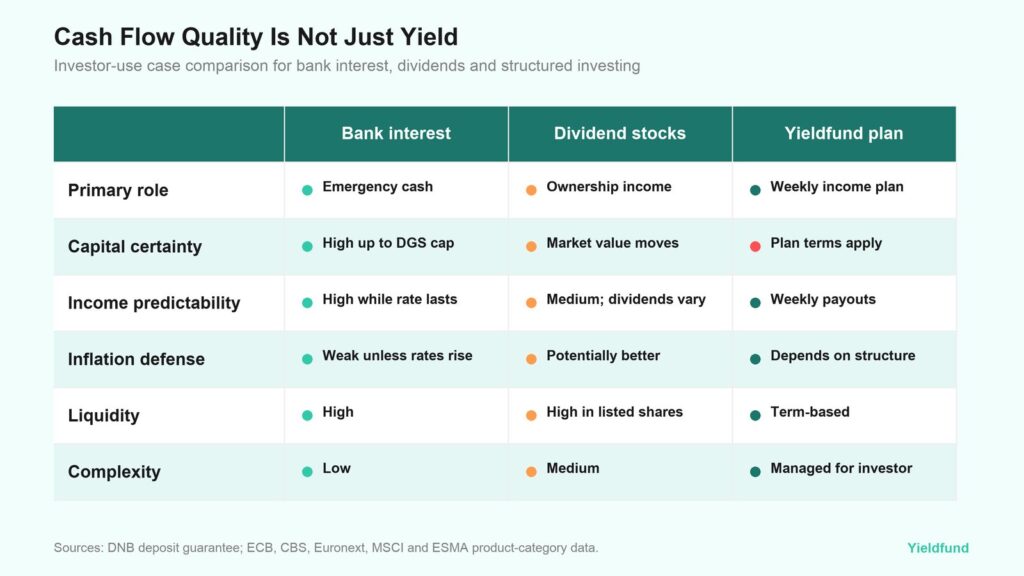

Bank interest is the simplest form of cash flow. It is transparent, liquid, and familiar. In the Netherlands, deposits are also protected up to EUR 100,000 per person, per bank under the Dutch Deposit Guarantee, administered by De Nederlandsche Bank.

That makes bank interest useful for emergency reserves, short-term savings goals, and capital that cannot tolerate market risk. The trade-off is income.

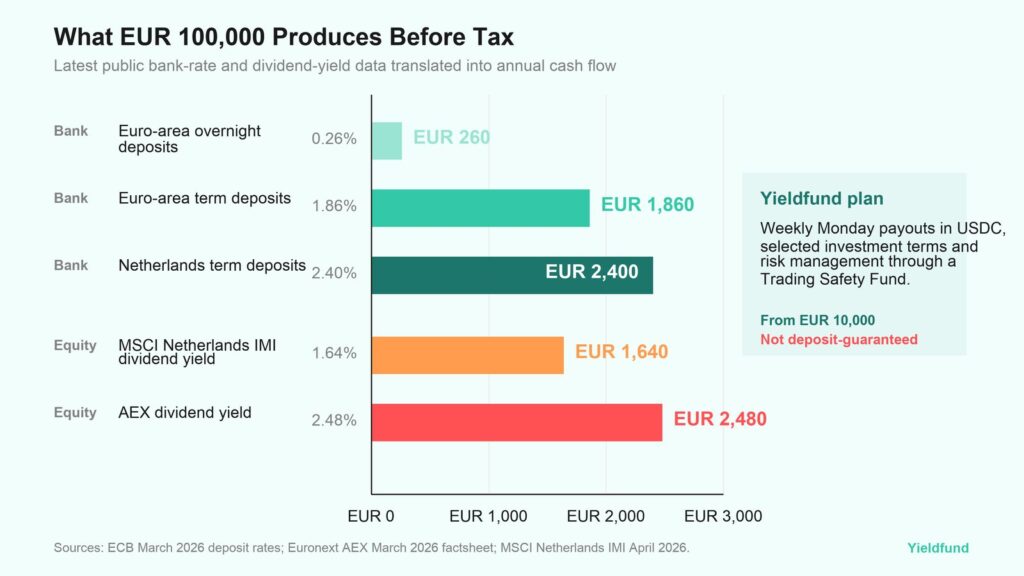

ECB data for March 2026 showed euro-area household overnight deposits paying 0.26% per year. Household deposits with an agreed maturity paid 1.86% in the euro area. In the Netherlands, household deposits with an agreed maturity paid 2.40%.

On EUR 100,000, that translates to roughly EUR 260 per year from euro-area overnight deposits, EUR 1,860 from euro-area term deposits, and EUR 2,400 from Netherlands term deposits before tax. That is useful, but it is not a full cash-flow strategy for many investors.

The key point: bank interest is strongest when the investor needs safety and liquidity. It is weaker when the investor needs income that can defend purchasing power over several years.

Dividend stocks: More potential but not sustained cash flow

Dividend stocks sit one step further out on the risk spectrum. They can generate income while also giving investors ownership in companies that may grow earnings over time. That makes dividends attractive for long-term investors who want cash flow and market participation.

The data is more nuanced than the marketing. Euronext’s AEX factsheet showed a dividend yield of 2.48% as of 31 March 2026. MSCI’s Netherlands IMI Index showed a dividend yield of 1.64% as of 30 April 2026.

On EUR 100,000, those yields imply roughly EUR 2,480 and EUR 1,640 of annual dividend income before tax and fees, if the yield were maintained. That can compete with bank term deposits, but the investor is taking equity risk. The dividend is not guaranteed, and the share price can fall much more than the annual income received.

There is also a concentration risk. MSCI reported that ASML represented 46.48% of the MSCI Netherlands IMI Index as of 30 April 2026. For Dutch equity exposure, this matters. A portfolio can look diversified by country while still being heavily exposed to a few large companies and sectors.

Dividend stocks can be powerful, but they are not cash substitutes. They are ownership assets that may pay income. That distinction is essential for investors who rely on portfolio cash flow.

Structured investing: Cash flow for set conditions

Structured investing approaches cash flow differently. Instead of relying only on a bank rate or a company’s dividend policy, the income profile is built into the investment terms. A structured investment may define a coupon, observation dates, maturity, underlying market exposure, barriers, and downside conditions.

That design is why structured products are often used by investors looking for income in uncertain markets. ESMA has noted that common structured retail product types in Europe include capital protection products, yield enhancement products, and participation products. ESMA also identified the search for yield as a driver of changes in product demand.

The market is not small. EUSIPA reported that sales of structured investment and leverage products in covered European markets reached EUR 46bn in Q1 2025, up 24% from the previous year.

Yieldfund is built around investment plans that pay weekly, rather than asking investors to wait for quarterly dividends or annual interest. Investors can choose a 1-year plan at 24% annually, a 2-year plan at 36% annually, or a 3-year plan at 48% annually. The plans translate into 2%, 3%, or 4% monthly interest, with payouts processed every Monday in USDC to the investor’s wallet.

That weekly rhythm payout is how Yieldfund, as a structured investment product, stands out. Bank interest may be credited monthly, quarterly, or annually, and dividends annually. Yieldfund, on the other hand, pays recurring interest weekly, and all the payment terms and transactions are visible through the investor dashboard.

The lower entry barrier is what makes Yiedlfund’s structured plan approachable. A minimum investment of €10,000 makes the product more accessible than many private or institutional-style income strategies. For investors comparing cash-flow options, this sits between a simple savings account and a more complex self-managed portfolio.

Yieldfund is registered with the AFM, but its investments are not protected in the same way as bank deposits. However, bank deposits under the Dutch Deposit Guarantee only cover up to €100,000 and typically offer lower yields. This raises the question of how investors should weigh capital allocation against risk.

The point is not that structured investing is automatically better than bank interest or dividend stocks. The idea is that Yieldfund provides investors a defined weekly cash-flow plan, with stated payout frequency, instead of leaving profits stagnant until investors decide it’s time to withdraw.

Which Creates Better Cash Flow For Investors?

There is no single winner. The better answer is portfolio design.

Bank interest is best for safety, liquidity, and near-term needs. It protects nominal capital up to the deposit guarantee limit, but the income may not be enough after inflation.

Dividend stocks are best for long-term investors who want ownership income and can tolerate volatility. They may provide better inflation protection over time, but dividends and market values can move.

Yieldfund’s structured investing product is best suited for investors who want a more intentional income sleeve, where the cash-flow terms are designed in advance. It can be useful when investors want weekly payouts, a selected investment term, and a predefined plan instead of relying only on bank rates or company dividends. But it requires understanding the conditions.]

The practical framework is simple. Keep emergency money in the bank. Use dividend stocks or equity funds for long-term market participation. Consider Yieldfund when the goal is planned weekly cash flow with defined terms, a lower entry point than many institutional-style strategies, and accepted product risks.

At Yieldfund, we believe cash flow should be built deliberately. Investors should not chase the highest yield in isolation. They should understand what creates the income, what can interrupt it, and what risk is being exchanged for it. That is where Yieldfund can add value: not as a replacement for all cash or all equities, but as a weekly income product designed to sit inside a broader cash-flow strategy.