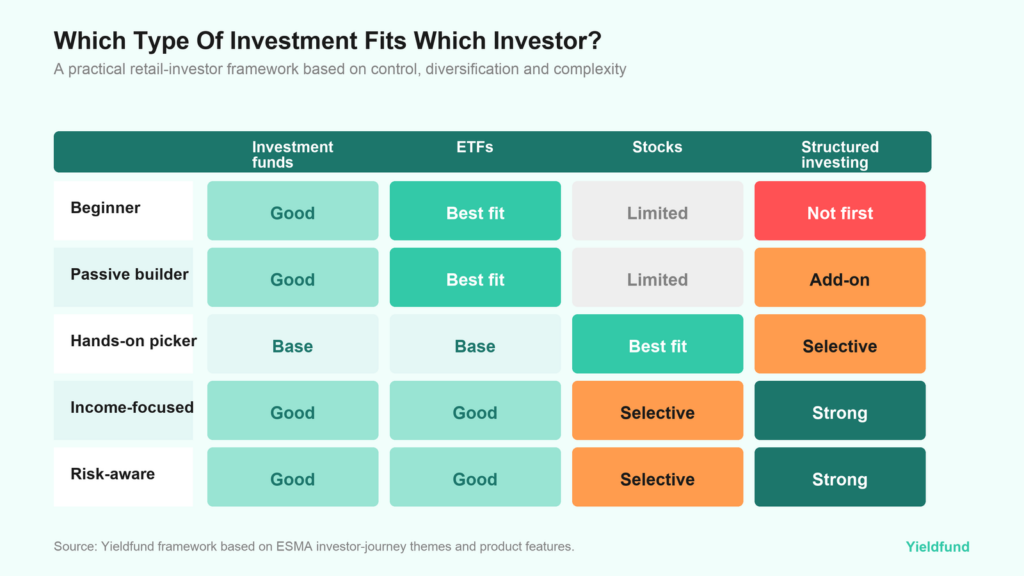

The main types of investments do not fit every investor in the same way. Investment funds and ETFs usually work because they provide diversification, while stocks suit already-experienced investors who can tolerate risk and conduct in-depth research. Structured investing can fit investors who want defined outcomes, planned income, or risk-managed exposure, but only when they understand the terms.

A better approach isn’t “which product is best” but rather which types of investments fit my skill set and knowledge.

The type of investment matters more

Retail investors ask the wrong questions: which product can earn the highest return, then work backward. A better starting point is to assess whether the product fits their experience, risk level, and time horizon.

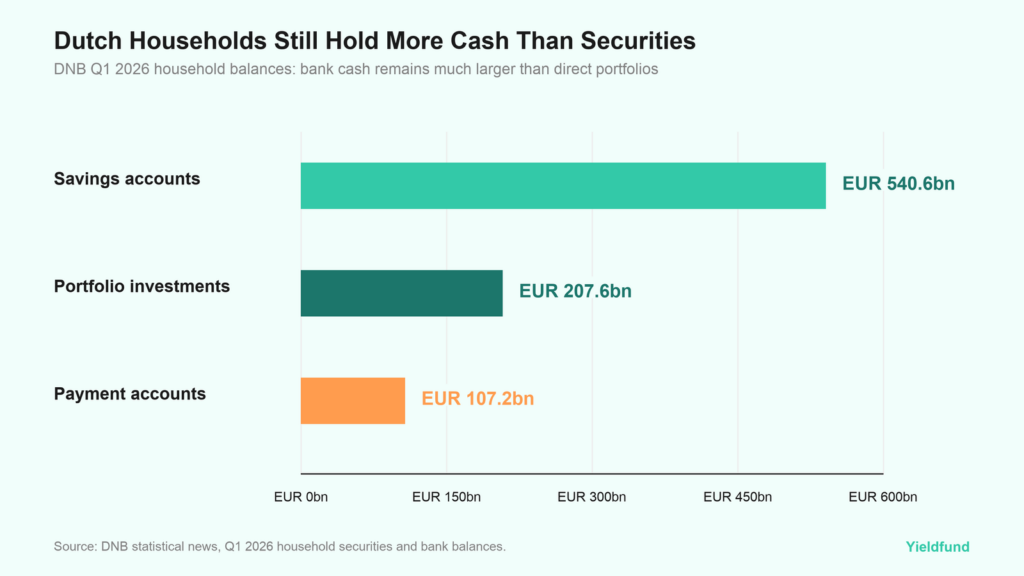

In the Netherlands, this matters because households still hold far more cash than investments. DNB reported that Dutch households held EUR 207.6bn in direct portfolio investments at the end of Q1 2026. The number is still below the €540.6bn held in savings accounts and €107.2bn in payment accounts.

Many people still prefer liquidity and certainty; secondly, the investing group needs clearer ways to choose among products. A beginner who buys individual stocks too early may take risks they do not understand. An experienced investor who uses only cash may miss the opportunity to protect purchasing power. The product should match the job.

Retail investors face barriers such as information overload, complex disclosures, low financial literacy, trust issues, fees, and tax complexity. Thus, people are not only choosing among products but also trying to understand a system that is often too hard to compare.

Investment funds: Best for investors who want professional allocation

Investment funds pool money from many investors and use it to buy a portfolio of assets. A fund might invest in global equities, bonds, real estate securities, dividend stocks, or a mix of asset classes.

For beginner traders, they are a good starting point because they eliminate the need to pick every security. They can also fit busy professionals who want someone else to manage allocation, rebalancing, and security selection.

The trade-off lies in the control someone has over the investment and in the starting point. Traditional investment funds in crypto require a minimum starting capital of €100,000, and the fund also selects where and how to invest. Retail equity fund ongoing costs fell by 8%, while retail bond fund ongoing costs fell by almost 15%. The decline is mainly driven by new funds entering the market with lower fees. Long-standing fund cost reductions were more limited.

Investment funds are a good fit when the investor wants diversified exposure and professional management, but less suitable when the investor wants maximum transparency and full control over every holding.

ETFs: Best for low-effort diversification

ETFs are one of the most beginner-friendly types of investments because they combine diversification with accessibility. Unlike traditional mutual funds, they trade on an exchange during the day, like a stock.

For a new investor, the main benefit is simplicity, as a broad global equity ETF provides exposure to hundreds or thousands of companies through a single product.

The ETF market is growing quickly in Europe. ETFGI data shows that European ETFs attracted $207.3bn in the first seven months of 2025, up from $127.2bn over the same period a year earlier. Assets in European ETFs reached a record $2.8tn by the end of July 2025.

Still, ETFs are not inherently safe, and investors need to make that distinction. A global ETF and a leveraged crypto ETF are both ETFs, but their risk profiles are completely different. Retail traders should look at what the ETF owns, how concentrated it is, what it costs, and whether it fits the holding period.

Stocks: Best for investors who can handle risks

Stocks are the most direct form of ownership in this comparison. When someone buys a stock, they own a piece of the company, and the stock can pay dividends, allowing investors to build a highly concentrated portfolio.

But stocks also demand the most from the investor. They need to understand valuation, business quality, competition, debt, management, earnings, risk, and market psychology. What this means is that they need to be able to handle volatility driven by market fluctuations without letting price moves lead to emotional decisions.

Only 27.6% of nearly 30,000 U.S. stocks from 1926 to 2025 outperformed the market. The median buy-and-hold return was -6.87%, so the takeaway for retail investors isn’t that stocks are bad, but rather that trading stocks is difficult without the necessary knowledge.

That makes individual stocks a better fit for investors who have time, discipline, and a reason to take concentrated risk. For beginners, stocks can still have a role, but usually as a smaller satellite around a diversified core of funds or ETFs.

Structured investing: Best for predictable income

Structured investing differs from funds, ETFs, and stocks because its return profile is designed around terms. A structured investment defines income payments, maturity, and market exposure while managing downside and risks.

Structured investments like on Yieldfund use a bond-like structure, where investors select a plan and receive fixed weekly payments to their wallet. The difference is that traders don’t have to trade themselves; instead, Yieldfund implements strategies and trades using its proprietary quantitative trading algorithms.

For inexperienced investors, companies like Yieldfund make it easy to access the crypto space and earn yields without having to trade manually. As investors become more drawn to consistent yields without the volatility, data suggest that structured retail product costs were broadly stable in 2024, while interest-rate-linked products reached 27% market share, up from just 1% in 2021.

That does not make structured investing a replacement for an emergency fund or a simple ETF portfolio. Structured products can carry liquidity risk, market risk, counterparty or platform risk, and terms that must be read carefully.

Structured investing is best suited as a defined sleeve within a broader portfolio, especially for investors who understand the terms or for retail traders who want exposure to crypto but don’t have time to learn to trade or the basics.

Which options fit which investor type

The easiest way to compare investment types is to map them to the investor level.

For beginners, the best fits are ETFs or structured investments because they provide a lower entry barrier. For beginners, the goal isn’t excitement but exposure, without having to deal with or understand volatility and complex terminology.

For passive long-term investors, ETFs are often the cleanest core. Investment funds can also work, especially multi-asset funds or managed solutions. The key is cost, diversification, and staying invested.

For hands-on investors, individual stocks can make sense, but only once they have a process in place. A stock portfolio without process is usually just confidence in disguise.

For income-focused investors, dividend funds, bond funds, selected dividend stocks, and structured investing can all play a role. The question is whether the income is reliable, what risk supports it, and how liquid the capital remains.

The bottom line on types of investments

The type of investment someone chooses depends on several factors, and, as we explored throughout the article, it’s not straightforward. We provided guidelines and suggestions on which product fits which type of trader.

Investment types are open to everyone, and investors should make decisions that minimize risk and preserve capital to build wealth. For a retail investor with time and some experience, the product fits differently from those of investors with minimal time and a willingness to learn.

Yieldfund is a quantitative trading company where investors can select an investment plan with returns of up to 48% per year, depending on the plan, and receive weekly payouts without having to manually trade the market or worry about crypto fluctuations.