Most investors invest too late because they typically wait for the perfect market moment, which never appears. When they in fact start, much of the opportunity may already be priced in. For retail investors, the real risk is not only buying at the wrong moment, but losing years of compounding while waiting for perfect certainty.

Reason why most investors invest too late

Most investors invest too late because they wait for certainty. They want the market to look safe, the headlines to turn positive, the chart to stop falling, and other people to confirm that the opportunity is real. The problem is that markets usually reward risk before the outcome feels obvious.

That is why late investing is not only a beginner’s mistake. It is a behavioral pattern. Retail investors often delay because they do not feel sufficiently educated, hold too much cash for comfort, wait for a better entry point, or act only after a stock, fund, crypto asset, or sector has already become popular. By then, the easy part of the move may already be gone.

The core lesson is simple: the risk of investing too early is immediately apparent, but the cost of investing too late is often hidden for years. A bad entry can feel painful next week. A lost decade of compounding only becomes obvious when the portfolio is too small.

The real cost of waiting to invest

The strongest argument against investing late is not motivational. It is mathematical. Time gives capital more periods to compound. Waiting removes those periods.

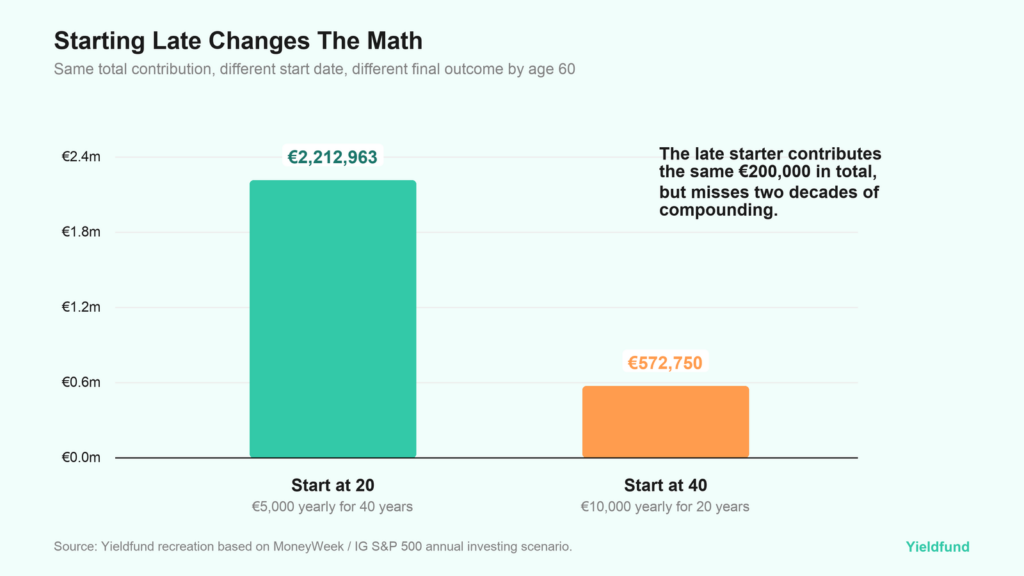

Suppose two investors contributed €200,000 to the S&P 500 by age 60. The person who started at 20 and invested €5,000 per year ended up with approximately €2.21 million. The person who started at 40 and invested €10,000 per year ended with about €572,750. It’s the same monthly contribution, but a significantly lower result if they started late.

This is why many investors regret waiting: investors with at least €10,000 in assets said they wished they had started earlier, while only half said they wished they had started earlier; what’s noteworthy is that half said it took them longer to become comfortable with investing.

The last remark matters for how retail views investing, as most people don’t delay it out of laziness.

They don’t prioritize investing because it feels emotionally expensive, and they have to invest far more than just money. The gap between being financially comfortable with risk and not is high. Cash, for many, feels safe and calm, while markets create uncertainty. Over a long period of time, inflation and missed compounding can make comfort feel very expensive.

Retail investors wait for confirmation

Retail investors with minimal knowledge often look for a signal that removes doubt, and they wait until the market has recovered, an asset is trending on social media, or a friend has already made money. That behavior is understandable, but it’s why retail investors invest later, and they end up not reaping the benefits of the market.

Beginners rarely have a framework for valuation, position sizing, or risk management. They use the crowd’s wisdom to borrow confidence, and that always arrives late. The retail landscape is changing even more, with Gen Z relying on social media, online sources, and other major channels for investment information. Social access can help people start, but it also creates a feedback loop: people hear about an investment after it has already produced a story worth sharing.

This is one reason retail investors often buy after a theme becomes obvious. AI, crypto, meme stocks, commodity spikes, and high-dividend shares all follow a similar path.

Market timing feels safe, but it creates a behavior gap.

Waiting for the right moment feels like risk management. In reality, it often becomes market timing. The investor says, “I will invest after the next drop” or “I will wait until volatility calms down.” Sometimes that works. Often, it leaves the investor watching from the side as markets recover without them.

The average U.S. fund investor earned 7.0% per year over the decade through 2024, while the funds themselves earned 8.2%. That 1.2 percentage-point annual gap was linked to the timing and size of investors’ purchases and sales. This is the hidden cost of trying to be clever with timing.

Retail investors may own good products but still earn weaker results because they add after strong returns, reduce exposure after losses, or pause contributions during scary periods. The phrase “time in the market beats timing the market” is overused, but the data behind it still matters. Retail investors do not need perfect timing to build wealth; instead, they need a repeatable system that prevents them from constantly waiting for emotional certainty.

Why buying late turns into overtrading

When investing too late, traders end up overtrading, which creates more risk than not investing at all. When someone enters after a big move, their positions are more emotionally fragile, and a normal price pullback can feel like proof they made a mistake. A small gain can feel like something to protect.

Instead of holding onto plans, investors with limited knowledge react to every move. And that’s a mixture of a lack of knowledge of how markets work and emotional uncertainty about their decision.

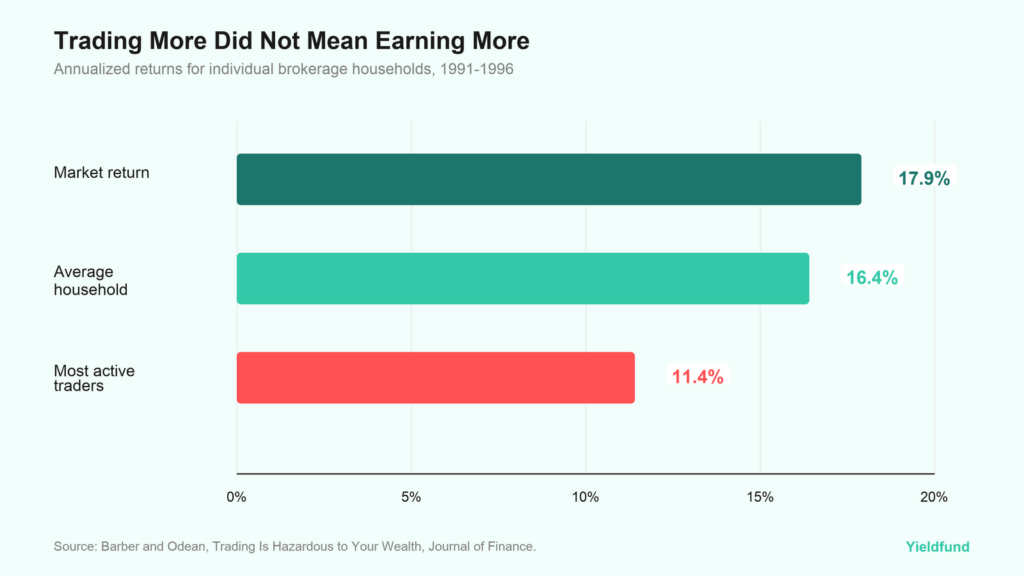

A study of 66,465 U.S. brokerage households found that the most active traders earned 11.4% annually, while the market returned 17.9% over the same period. The average household turned over 75% of its common-stock portfolio annually. Activity felt like control, but it reduced returns.

For beginner traders, it matters because a late entry and high activity reinforce each other. When an investor waits too long, buys after momentum, becomes nervous, sells quickly, then waits again. It all leads into a portfolio driven by headlines and emotions rather than a time-based horizon. It’s not that every trade is bad, but that many retail traders use trading to cope with the anxiety of not having a plan. That is an expensive substitute for strategy.

Investing early without taking risks

The answer is to replace emotional timing with rules. First, separate emergency cash from investment capital. Money needed for rent, debt payments, taxes, or short-term obligations should not be forced into volatile assets. Once that buffer is defined, the remaining capital has to be allocated to avoid losing it to inflation.

The second rule is to have a defined allocation, which means investing a fixed amount every month or a fixed percentage of income after cash needs are covered. What this does is remove the necessity for a decision that creates friction between being ready to invest and timing the market.

Third, separate core investing from speculative ideas. A beginner can keep most long-term capital in diversified exposure and reserve a smaller amount for higher-risk themes. That structure reduces the chance that FOMO becomes the entire portfolio.

Structured investing to invest early

Having cash is always useful in the moment, and waiting can be rational if the money is needed then. But waiting indefinitely because the market feels uncertain is not a strategy; it’s a decision to let fear control the entry point.

Investors are emotional, and that often leads them to invest late because they don’t want to make the wrong decisions or, worse, lose the money they worked for. What many fail to understand is that inflation is present and affects purchasing power.

Yieldfund provides a way for retail investors who are unsure of how, where, and when to invest to diversify their portfolio and earn from the performance of Yieldfund’s quant trading platform. Depending on the chosen plan, investors can earn up to 48% yearly returns and receive weekly payouts.