When you look at cash and inflation, for many investors, they’re moving in opposite directions. While cash may seem safe because the balance isn’t moving, inflation erodes the purchasing power of Dutch households’ spending.

For new investors, it’s the first lesson that risk isn’t about losing money but about missing out on gains from rising inflation.

Why does holding cash continue to feel safer?

Cash is always safer because it has a nominal value, and holding it won’t create any friction. This means it won’t increase or decrease in value the next day. Why it feels safe for most people isn’t because its stability is predictable for covering daily expenses, emergencies, and bills. But that doesn’t mean the amount you bring home remains the same.

What people fail to understand is that cash safety isn’t the same as income safety. Income means buying the same things repeatedly without being affected by external factors. But with inflation increasing, the value of your real income decreases. A modern culprit is for people to hold money in savings accounts that pay 0.13%, even though inflation has increased. Recent data shows inflation in the Netherlands has increased to 3.5%. For someone who makes the same amount, their real income drops.

This is why the cash vs inflation question matters in the Netherlands in 2026. Interest rates are no longer zero, but inflation has not disappeared. The result is a gap between feeling safe and actually staying ahead.

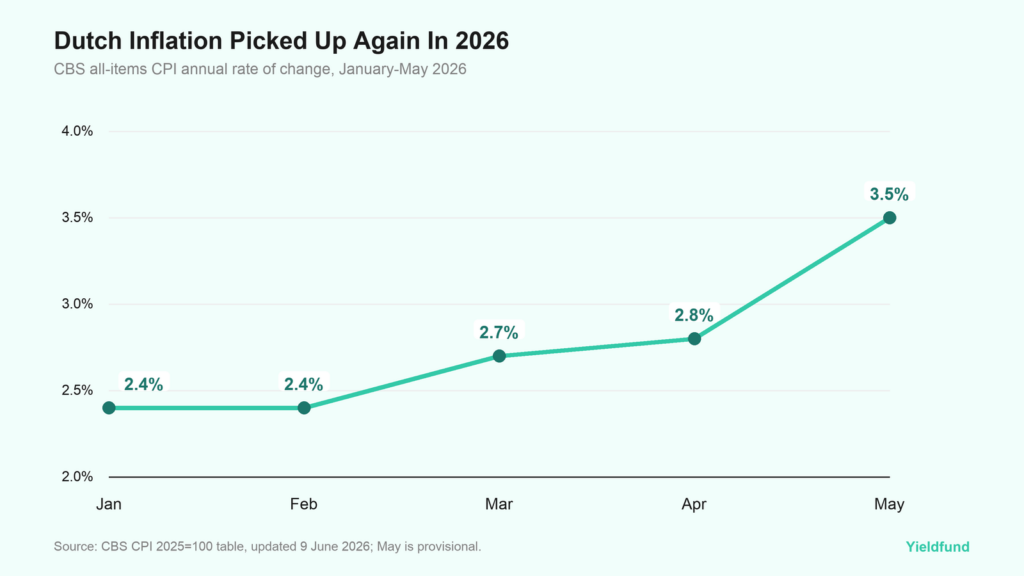

Dutch Inflation In 2026: What the latest CBS data show

Dutch inflation picked up again in the first half of 2026, and CBS data shows a CPI inflation of 2.4% in January and 2.7% in February. In May, inflation numbers increased to 3.5%, and while the figure is provisional, it’s still the largest inflation published in over a year.

For Dutch households, higher inflation put pressure on everyday spending, and real income suffered. While the 3.5% increase isn’t felt fully in the first months, it will continue to show up as higher rent, food prices, service costs, and ultimately, potentially a lower purchasing power. Even when headline inflation is lower than the 2022 energy shock, prices can still compound faster than cash income.

The Dutch economy is also a useful case because households traditionally hold large cash buffers. That is rational after years of housing-cost pressure, tax uncertainty, and rising living expenses. But when inflation is above most savings returns, the cash buffer needs a purpose. Otherwise, money that feels protected can quietly lose real value.

The real returns on savings: Cash vs inflation

To understand your financial position, use this simple calculation: Real Return = Interest Rate – Inflation. If inflation is higher than your interest rate, your real return is negative. ECB data shows that in April 2026, Dutch household deposits paid 0.13%, while fixed-term deposits reached 2.45%. By comparison, euro-area household overnight deposits paid 0.26%, while euro-area fixed-term deposits paid 1.91%.

What’s interesting is that the Dutch inflation of 3.5% is putting all cash rates below inflation, so anyone who made cash deposits is losing money. While this doesn’t automatically mean that savings accounts are useless, it does show how cash can lose some of its value in a matter of months. It becomes less effective as a long-term wealth strategy when inflation exceeds the yield.

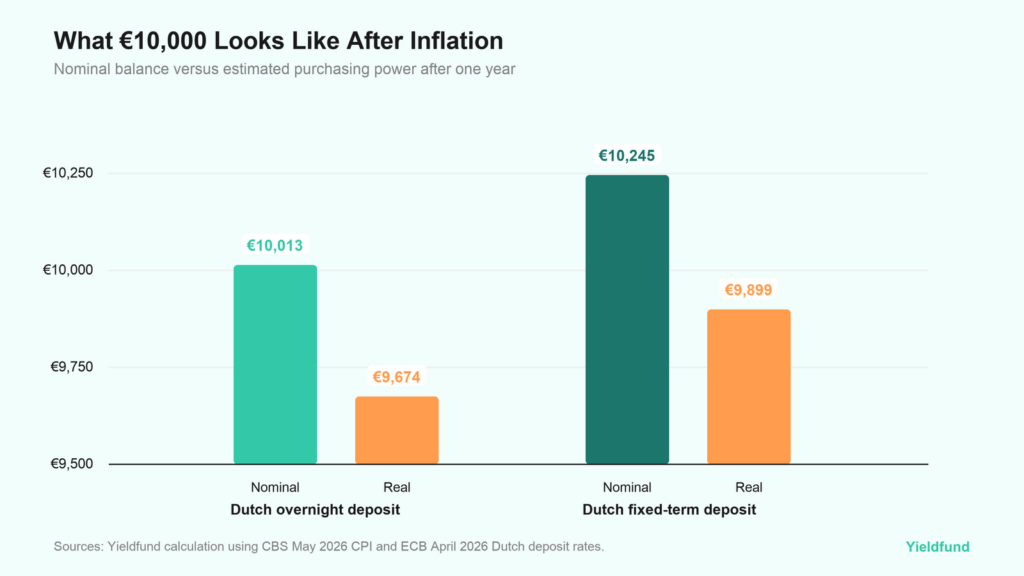

How inflation affects a €10,000 deposit in one year

At the Dutch overnight deposit rate of 0.13%, €10,000 grows to about €10,013 before tax after one year. But if prices rise by 3.5%, that balance has purchasing power of roughly €9,674 in today’s terms.

At the Dutch fixed-term deposit rate of 2.45%, €10,000 grows to about €10,245 before tax. Adjusted for 3.5% inflation, the real purchasing power is roughly €9,899. That is much better than an overnight deposit, but still slightly negative in real terms.

This is the beginner-friendly way to think about cash and inflation. Your bank balance answers one question: how many euros do I have? Inflation answers another: what can those euros buy? While the fixed-term account is a better tool, both options still leave you slightly behind in real terms.

Households rely more on cash in the Netherlands

Dutch households hold a lot of cash-like assets. CBS household wealth data show that private households held €444.4bn in bank and savings credits in 2024, up from €429.2bn in 2023. By comparison, household securities were €173.5bn in 2024.

This is not irrational. Cash is psychologically useful. It gives people a sense of control when life feels expensive. In the Netherlands, households also face big-ticket financial decisions: rent, mortgages, childcare, energy bills, insurance, student debt, and taxes.

But the same data also shows why the conversation around investing in the Netherlands audiences needs to be practical, not ideological. The point is not that every euro should be invested. The point is that every euro should have a role.

Emergency cash has a job. Money for a home purchase comes from a job. Tax money has a job. But long-term surplus cash sitting at a low rate is doing a different job: quietly absorbing inflation.

How to handle allocation when it comes to cash and inflation

Preventing real income from falling requires some strategic capital allocation. It’s often covered under money management and has to be divided based on the time horizon for which the money is needed. For cash that needs to be available in the short term (the next few months), investors need to protect the nominal value first. For example, having an emergency fund is encouraged and should include 3-6 months of living expenses.

In that case, inflation has minimal impact,, as 3.5% inflation wouldn’t have a significant effect on the value of income in the near term. But cash can become expensive to hold when it’s used for goals with longer time frames. That means that keeping too much cash in low-interest accounts can be both risky and expensive. Especially with inflation continuing to grow.

From our experience, managing money requires people to have two things in mind: the frame and the risk factor. When we covered the 50-30-20 rule, that provides a good framework for beginner investors. A large portion of the income has to be set aside for mandatory expenses; 30% for non-mandatory expenses while the remaining 20% is allocated or invested.

The framework isn’t bulletproof by any means, but can be adapted to individual cases. While it does not remove risk, investing involves volatility and possible loss. At the same time, holding cash comes with risks as well.

How investors can protect purchasing power

The goal for any investor is to switch the mentality from preserving cash to building capital. It’s an often-overlooked strategy that can be understood and implemented once people grasp how inflation affects capital.

To protect purchasing power, investors need to understand the inflation rate. Banks often offer lower interest rates, or, if there are high-interest accounts, they match inflation. As we’ve seen in 2026, inflation is continuing to rise, and as geopolitical events unfold, it won’t stop anytime soon.

What’s important is to compare the nominal and the real value of the returns. A 2.45% deposit rate sounds good compared with the zero-rate years. But if inflation is 3.5%, the real return is still negative before tax. That gap should shape the decision.

Protecting purchasing power to a certain extent has the same characteristics as building wealth. Investors need a set strategy to manage risks. It’s better to build wealth more slowly and safer to avoid running your savings into the ground. For that, investors could allocate based on risk levels. This means:

- Assign a purpose to every euro: If it’s for next month’s bills, keep it in cash. If it’s for a ten-year goal, look beyond the savings rate.

- Build gradually: Don’t make all-or-nothing investments. Rather, investments should be recurring to avoid emotional investing.

- Keep risk controls visible: Always ask about the expected return and the underlying risks.

Cash and inflation need to be understood and used in the current economic context. In 2026, cash is a tool, while inflation is the test that shows whether that tool is being used for the right job.

Yieldfund, provides ways for investors to diversify their portfolios and access crypto yields without having to trade themselves. Investors can opt for investment plans of up to 48% returns depending on the chosen contract and weekly payouts.