What makes more sense between a mortgage overpayment and investing in the Netherlands heavily depends on the mortgage type and the time horizon, as a low mortgage rate over a longer time horizon makes investing better in the long term.

For Dutch homeowners, ECB rates going higher means they might have to reconsider how they approach the question based on the revised interest rates. So what’s better, paying the mortgage upfront or investing the capital?b

Should you overpay mortgage or invest?

Overpaying the mortgage should be calculated based on how much you are saving. If overpaying saves you 3-4% in interest (after paying taxes), then the remaining capital needs to provide higher returns.

Investments need to beat the return after taxes, fees, and inflation. What’s worth noting is that few people are able to achieve that with the limited time they have. What investors need to understand is the following: if the mortgage is fixed, over 10-20 years, investing the surplus can still make sense. Any additional yield you generate will be better for your wealth.

However, if the mortgage is expensive and fluctuates with inflation, then what makes sense is overpayment. That’s because in the initial period, people who used banks to finance their home are paying more on interest than on the main loan.

When someone holds cash, it feels safer, but with inflation higher, it loses purchasing power. Overpayment then delivered better returns through avoided interest. The right answer in that case is: pay early if you have a variable mortgage, invest if the mortgage is low and fixed.

What if ECB rates remain high? What’s better?

ECB interest rates can change the decision because mortgage rates, savings and the costs of holding cash become more expensive. When mortgage rates were 1% – 2%, or even negative during and prior to the COVID crash, returns always beat them on a long horizon.

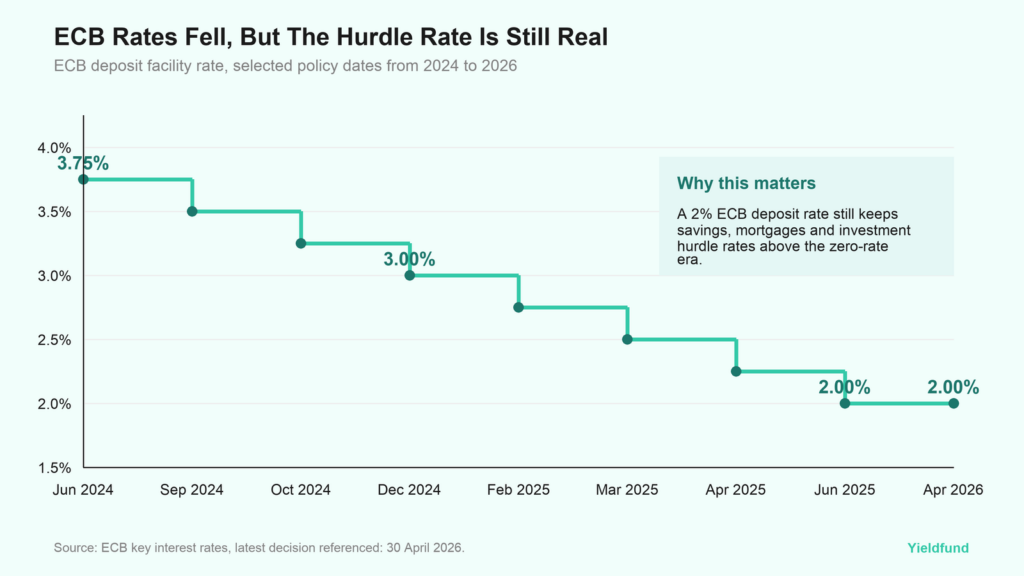

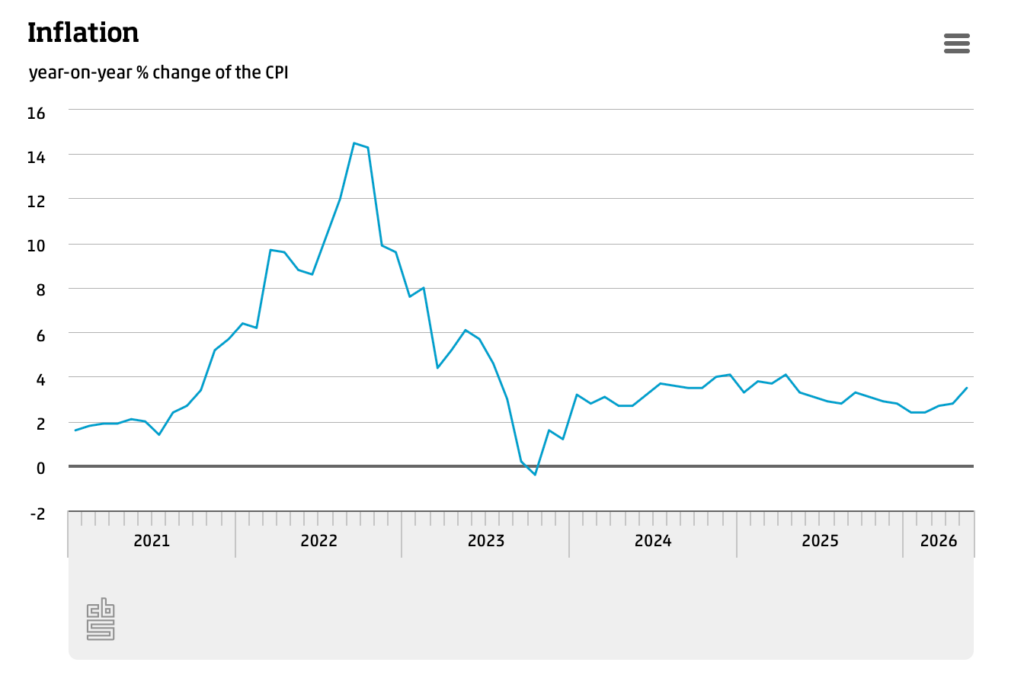

Looking at the economic situation now, the hurdle is more percentage points due to inflation. Over the past two years, inflation rates have been high. In April 2026, the ECB announced they are keeping rates unchanged at 2%, 2.15% for the main refinancing. Rates have decreased from 2023 (4%) but they haven’t returned to zero.

Even mortgage numbers tracked the same path, with the average Dutch 10-year fixed rate reaching 3.83% in late 2025. Additionally, the 20 and 30-year fixed deposits at 4.24% and 4.39% respectively. When you look at the 1-2% rates of the late 2010s, that’s a 2-3% higher cost for having a mortgage.

How Much You Get From Overpayment

Paying the mortgage early means you’re not paying such a high interest. For a 30-year mortgage, people pay on average 1.8x the borrowed amount. In the first 10-15 years, they pay more for the interest than for the main amount.

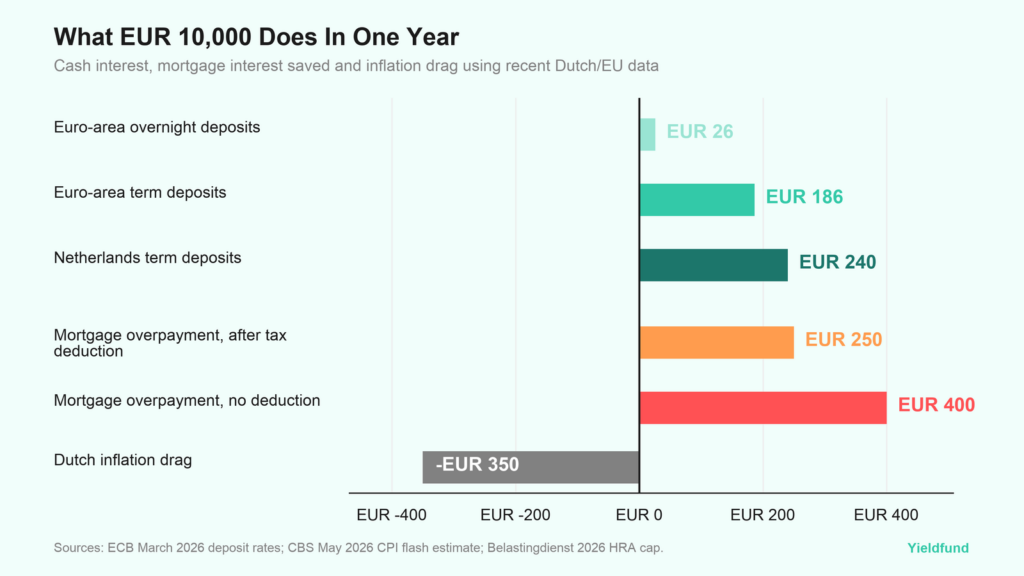

For example, if you overpay €10,000 on a 4% mortgage, the gross interest you’re saving is €400 per year. That number is fixed, assuming the loan allows extra repayment.

In the Dutch tax system, mortgage interest deduction is capped at 37.56% in 2026, so if your mortgage interest is deductible, overpaying helps reduce the amount of interest you can deduce.

Then, a 4% deductible mortgage therefore behaves more like a 2.5% net benefit. On a €10,000 repayment, that is roughly €250 per year rather than €400.

How Dutch Tax Changes The Calculation

For Dutch homeowners, mortgage interest is deductible in box 1, but only at a capped rate. The Belastingdienst caps the deduction at 37.48% in 2026. If your interest is deductible, overpaying reduces both the interest you owe and the tax relief you receive. A 4% deductible mortgage therefore behaves more like a 2.5% net benefit. On EUR 10,000, that is roughly EUR 250 per year rather than EUR 400.

While penalties aren’t fully transparent, they can still hurt the economics. In the Netherlands, banks allow overpayment of 10% of the loan amount per year without penalty. This makes sense when thinking about how to compare both paying upfront or investing.

If the mortgage is not deductible, or if the loan is an investment property loan without the same relief, the saved interest can be closer to the full gross rate. That is why two investors with the same mortgage rate can reach different decisions. This applies to second homes or buy-to-let properties.

How does holding cash compare with overpayment?

Every person still needs some cash for an emergency buffer, but it should be calculated. Every Euro above is paying inflation at a premium since inflation reached 3.2% in May 2026 – up from 3% in April.

Bank deposits are also below inflation numbers, with ECB data showing daily deposits are paying 0.26% while longer-term deposits with a higher maturity only pay 1.86%.

With inflation at 3.5% as of May 2026 in the Netherlands and term deposits paying only 2.4%, people are losing approximately 1% for holding onto cash. While cash can be necessary, it can be expensive to hold.

Box 3 taxes make holding cash expensive

For Dutch residents, the box 3 wealth tax is an extra cost for holding cash and investments above a certain tax-free limit.

For 2026, the Dutch tax office assumes your bank deposits earn about 1.28% and your investments earn 6.00%. This assumed income is then taxed at 36%, although you have a tax-free allowance of €59,357 (€118,714 for couples).

This means that any cash you hold above the threshold loses value due to inflation and you get a tax bill for it, even if you earn less interest than the tax office assumes. However, overpaying your mortgage reduces your debt instead of counting as taxable wealth, making it a potentially better option after taxes.

When Does Investing Still Beat Mortgage Overpayment?

Investing could be better than paying off the mortgage early when you can tolerate drawdowns without being emotional and you have a low-rate mortgage. In the long-run, equity returns have historically been higher than current Dutch mortgage rates.

European stocks have had a strong year with the STOXX reportedly returning 20.6% in 2025 – mostly attributed to a few AI companies. A single profitable year isn’t the same as across a decade, as major asset managers like Blackrock publish long-term capital market assumptions in the mid-to-high single digits for developed-market equities. These end up being closer to typical mortgage rates than the 2025 headline suggests.

Most people who look at whether to pay off mortgages only look at the past year’s performance, without considering the longer time frame. So overpayment delivers an avoided interest cost. Equity returns come with valuation, earnings, currency and drawdown risk and require more analysis and understanding of the market to stay profitable.

That does not mean retail investors should avoid markets. It means the hurdle has risen. A long-term ETF portfolio can still justify the volatility. A short-term trade often cannot.

Overpayment or Investment?

When overpaying mortgages wins:

- The mortgage rate is high, variable, or close to refinancing.

- Interest is not deductible, or deduction is capped low.

- The time horizon for the money is under five years.

- Reducing debt would move you into a better loan-to-value bracket.

When investing wins:

- The mortgage is low-rate and fixed for many years.

- The emergency buffer is already in place.

- The money can stay invested through a 30–50% drawdown.

- Box 3 considerations and time horizon both favour productive assets.

Smart capital allocation

Holding a mortgage in Europe means you’re relying on the ECB rates. With rates higher at 4%, it means the expenses you incur aren’t just a household bill, it means that every euro you are able to save needs to reduce debt and earn a high enough return to justify the risk. If you’re investing, people should feel comfortable or understand the risks. If you’re paying the mortgage off early, you should understand the penalties, the money you’re locking away, and what you’re missing.