The US/Iran conflict is far from over, yet it has managed to create economic distress. As global supply lines and oil stocks get depleted, in 6 months the global economy could be a lot worse than we imagine it to be. Even as oil headlines would have cooled, shipping through the Strait of Hormuz would be partially restored and central banks would be discussing recovery rather than conflict.

The aftermath of the conflict can look different depending on how the conflict will evolve and whether new escalations will occur. Damages inflicted by the shock operate on delays, with some channels requiring months to years. The global economic situation at the end of the year will be shaped by past disruptions that are still affecting the system.

You can already see the shape of that aftermath in current forecasts. Energy prices will be lower but not normalized. Food inflation will be accelerating just as energy inflation subsides. Refining and shipping costs will have established a structurally higher baseline. And the European economy, with the Netherlands serving as a clear example, will carry a thinner growth cushion into 2027 than it had entering 2026.

From headlines to economic reality

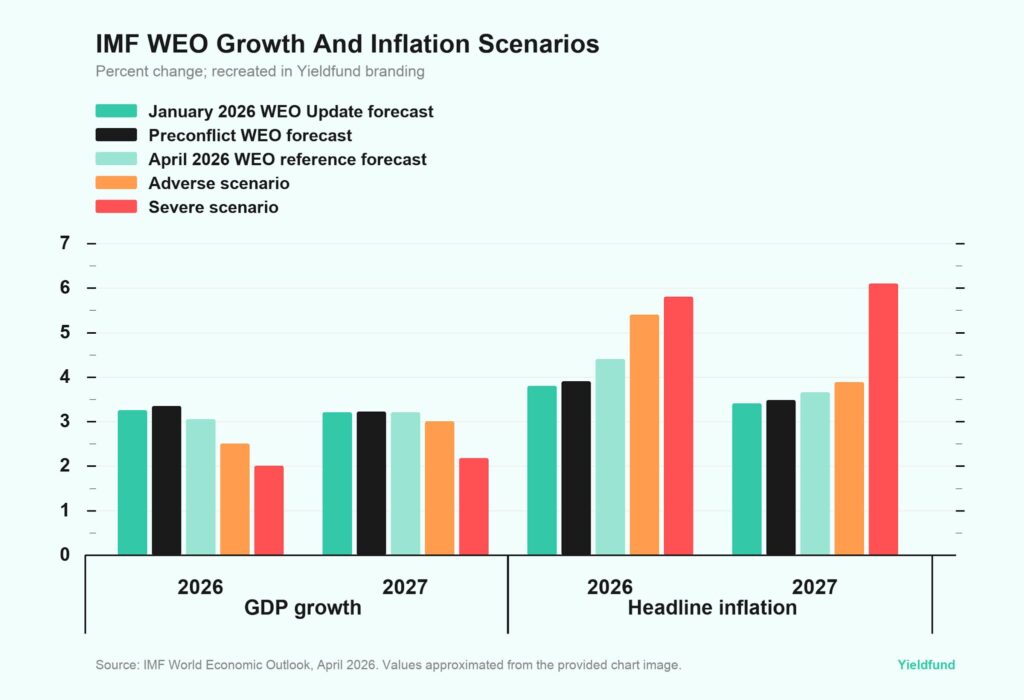

In 6 months, the conflict will have transitioned from price outlooks into the balance sheets of households and governments. IMF outlooks project global growth at 3.1% in 2026, while in Europe projections are set at 1.1%, if the conflict doesn’t escalate. This means brent oil prices remain the same and the shock remains contained. The current projects are already revised down from late-2025 expectations.

In 6 months, capital expenditure plans paused in Q2 and Q3 will not have fully resumed. This in turn will mean business confidence will be below pre-conflict levels while saving rates will continue to drop as consumers will have to manage higher utility and grocery bills. In Q4 of 2025, household savings had already decreased by 0.4% in the EU due to other macroeconomic events.

While not dramatic, this creates a persistent, cumulative drag that pushes recovery into 2027 rather than the second half of 2026 that consensus had anticipated last year.

Energy markets remain a core problem

The more important metric that will create issues is the energy market. The underlying structural costs would not have normalized by the end of 2026. Brent prices will not ease as aggressively as they spiked. The EIA underlines that prices could ease from $106 in June to approximately $79 in 2027, if the conflict isn’t escalating or continuing and oil production can recover.

A report by Goldman Sachs reinforced the price prediction, as countries will look to rebuild their strategic oil reserves. The forecasts for 2026 are dependent entirely on a few moving factors which could persist even after crude prices soften.

Europe’s refining capacity and inventories. Europe’s ARA hub will have operated through 2026 well below normal levels for two reasons. Refiners depleted stocks to compensate for lost Gulf crude, and several European refiners that were already on the edge of closure used the high-margin period to harvest profits rather than reinvest.

S&P Global identified before the conflict that European refining is experiencing a long-running attrition cycle due to high compliance costs. These increased from $0.60–0.80 per barrel today to $3–4 per barrel by 2035 and the Gulf conflict only accelerates this trend. By November, Europe enters heating season with thinner diesel and gasoil buffers than at any point since 2022.

War-risk insurance. Pre-conflict Hormuz transit insurance operated around 0.25% of vessel value. New quotes will not shrink and remain elevated at $3-8 million per large tanker. The base case suggests that premiums will have eased by only 1-2% as insurance companies need stability before fully repricing. This will still mean they will be four to eight times higher than pre-conflict levels. This cost transfers directly into refined-product prices and freight rates.

OPEC+ cohesion. The conflict accelerated a fracture that was already developing. Wood Mackenzie has identified the UAE’s movement away from the formal OPEC+ structure during the crisis, weakening the ability to defend prices when demand softens. This signals bearish implications for oil in 2027 but bullish for volatility as future shocks will reprice faster and overshoot more significantly.

Inflation is becoming the bigger risk

The most important shift between now and the end of 2026 will be the transition from energy inflation to food inflation. Energy inflation is projected to peak in Q2 and decrease in Q3 due to “base effects.” The ECB models energy inflation could turn negative in 2027 while food will only start its cycle.

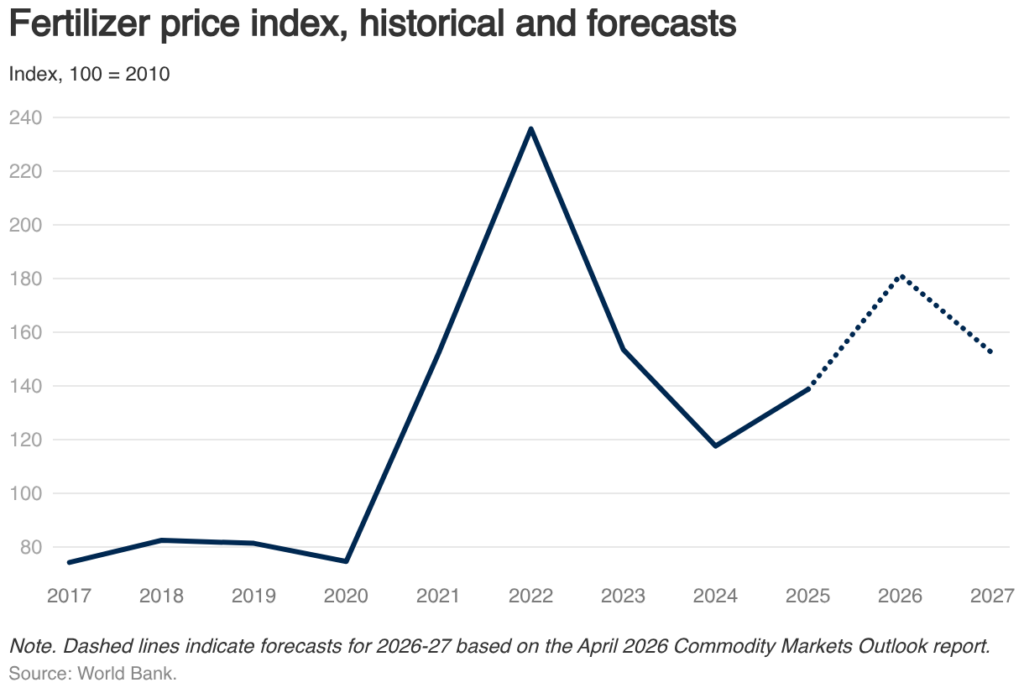

The delay in inflation points is mechanical as fertilizer prices are expected to increase by 30% in 2026. The closure of the Strait of Hormuz disrupted more than just oil. It also created a shortage in nitrogen and phosphate fertilizer trade.

The spring 2026 planting season used more expensive fertilizer, sometimes less of it, and in some emerging markets, simply less land was planted. These decisions manifest in 2026/27 crop yields and in food prices on a six-to-twelve-month delay.

In Europe, data from RaboResearch emphasize that food price inflation is expected to increase throughout 2026 and intensify in 2027. Data suggests food inflation in the Euro zone at 5-10% in 2027, while in other countries it can increase further. The mechanism is that European food retailers set prices annually, so most of the 2026 input-cost shock will be locked in during late-2026 contract negotiations and become visible on shelves in 2027.

This timing matters for the end of the year because central banks will be making rate decisions while energy inflation fades but food inflation begins to accelerate. ECB projects already show revised HICP up to 2.3% in 2026 and 2.2% in 2027 due to higher energy costs that feed into food and services which currently lag.

The risk in November is not runaway wages but sticky core inflation that prevents the ECB from cutting as quickly as both growth and energy data alone would justify. The most likely scenario shows euro area headline inflation returning toward 2.5%, but core stuck near 2.3% and food inflation accelerating into a 2027 peak.

Europe faces a direct squeeze

The aftermath in Europe can be more severe because the region absorbs the energy shock, the food shock, and delayed monetary easing simultaneously, on top of a weak growth starting point.

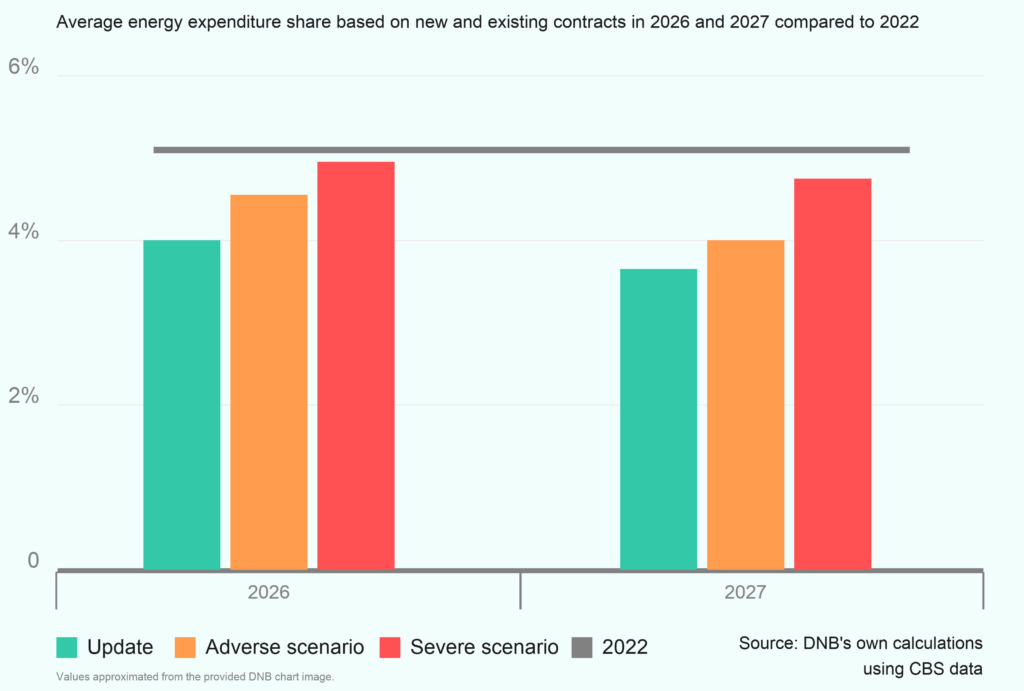

The Dutch GDP is projected at 1.3% in 2026, with elevated services inflation through 2025–26, and recovery only in 2027. This forecast was made before the full conflict shock was incorporated and the DNB scenarios show Dutch growth approximately 0.5% lower and inflation around 1 percentage point higher in the adverse case for both 2026 and 2027.

This means that disposable income will be affected by roughly 1% from higher energy costs in DNB’s limited scenario, scaling to 6% in the severe case. Export-exposed Dutch sectors such as logistics, refining, chemicals, food processing, and machinery, will be reporting weaker order books for early 2027.

The corporate refinancing wall, which the eurozone had been managing relatively smoothly, will face materially tighter conditions because the ECB has not cut as much as expected and credit spreads have widened due to growth concerns.

For many Dutch residents, real incomes are still recovering from 2022, mortgage costs are not yet meaningfully lower, and a new round of food-price increases are just starting. While none of these individually reaches crisis levels, together they push consumer confidence and consumption deeper into precautionary mode.

The forward conclusion

The aftermath of the US/Iran conflict in November 2026 does not mark the moment the shock ends. It represents the moment when the second wave will affect global economies.

While energy inflation has passed its peak, costs for refined products, freight, and insurance are still structurally elevated. The fertilizer shock from spring 2026 is now impacting crop yields and raising food prices, with European food inflation projected to be 5–10% in 2027. Although wages have not spiraled, core inflation remains too sticky for the ECB to cut rates as quickly as the weak growth outlook would otherwise warrant.

Here’s how to understand the next six months: the global economy will appear to have absorbed the shock, but it will be absorbing it for longer than forecasts written in late 2025 assumed and Europe ends 2026 with weaker than projected growth.